)

Life Insurance Corporation (LIC), the country’s largest insurer, could be the most valuable Indian company at Rs 4.5-5 lakh crore if it debuts on the bourses, as bankers have suggested to the Union finance ministry.

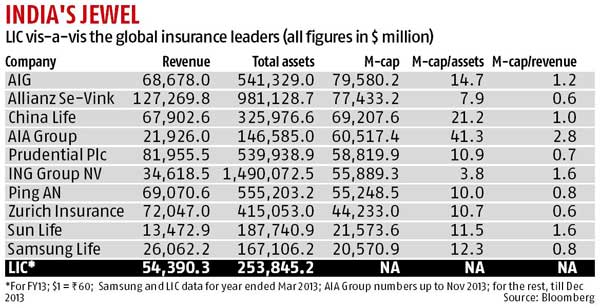

In 2012-13, the latest year for which data are available, LIC reported a revenue of Rs 3.26 lakh crore ($54.4 billion) and Rs 15.2 lakh crore ($253.9 billion) of assets under management. In 2013-14, the state-owned LIC reported first premium income of Rs 90,123.8 crore, a rise of 17.8 per cent over 2012-13 and a key metric for valuing insurance companies. Private Indian insurance companies, on the other hand, saw a four per cent drop in new premiums to Rs 29,517.4 crore in 2013-14.

Asian insurance giants like the AIA Group and China Life Insurance are, respectively, valued at around 41 per cent and 20 per cent of their assets under management. In slow-growing Europe and North America, insurers typically are valued at 10 per cent of their assets under management. American International Group (AIG), the world’s largest insurance company, is valued at 15 per cent of its assets under management (AUM). Taking an average of the shares of Asian insurers’ valuation in their respective AUMs as a yardstick, LIC’s market value is likely to be Rs 4.5-5 lakh crore.

At this valuation, floating 10 per cent of the LIC stock would fetch the government around Rs 50,000 crore. Analysts said an issue of this size would squeeze the secondary market and participation by retail and foreign institutional investors would be key.

“Life insurance companies, like mutual funds, are valued on their assets under management, their key source of revenue and profit. LIC will get a premium for being a market leader and for its huge investment portfolio accumulated over the past six decades,” said G Chokkalingam, founder of Equinomics Research Advisory.

In 2012-13, LIC’s investment income was Rs 1.04 lakh crore and miscellaneous income Rs 21,243 crore. It reported a surplus of Rs 1.49 lakh crore after paying all expenses, including claims, commissions, management and employee expenses and a five per cent valuation surplus to the government.

Tata Consultancy Services (TCS), currently India’s most valuable company, is worth around 4.31 lakh crore. It is followed by Oil and Natural Gas Corporation (Rs 3.65 lakh crore). In revenue, LIC ranks only below Indian Oil Corporation (Rs 4.93 lakh crore in 2013-14) and Reliance Industries (Rs 4.43 lakh crore).

Conservatively, LIC can be valued at 3-3.5 times its first-year premium income, a typical valuation matrix for insurance companies. This pegs LIC’s market valuation at Rs 3-3.5 lakh crore.

“Life insurance companies (can also be listed) according to their appraisal value, which is a multiple of their first-year premium income. This is likely to be high for LIC, given its low expense, high market share and nationwide network,” said Ashvin Parikh, managing partner, Ashvin Parikh Advisory Services LLP.

Listing LIC, though, will not be easy. It was created in 1956 through a law and follows an accounting method that is different from private insurers. Before listing, it needs to be corporatised if the suggestion by bankers to the finance ministry is accepted. The proposal is for the government to hold 51 per cent in LIC and divest the rest.

Senior executives and a former chairman of LIC, however, said it would not be an easy process. A former managing director of LIC explained that when the government had earlier considered listing LIC, the trade unions had objected, citing pay and pension benefits available to government employees.

Another issue, the executives said, was the appointment of LIC’s senior management team, which is currently approved by the government. That, if the insurer is listed, will have to be done after shareholder approval. “This may require an amendment in the LIC Act to allow shareholders to take a call on appointment issues, though it may still largely be decided by the government,” said a former LIC chairman.

Transparency and additional disclosures were what would be the major game-changer, said former LIC executives. “Large equity and debt transactions conducted on a daily basis are not disclosed, since it is not mandatorily required. Once LIC is listed, this will undergo a change and we are not sure if the staff will be comfortable with the move, since there could be fears about particular investment decisions being questioned. So, listing proposals are easier said than done,” said a former LIC executive.

In 2004, the All-India LIC Employees Federation had expressed concerns over a report by an accounting firm that proposed corporatisation of LIC and a possible listing. Some provisions also related to withdrawal of government guarantees on LIC policies. The Malhotra committee report had in 1994 proposed a similar concept for professionalising the insurance sector.

According to the LIC Act, there is a sovereign guarantee on its policies. The Act says the sum assured by all policies issued by LIC, including any bonuses declared, will be guaranteed as to payment in cash by the central government. Hence, former LIC executives said, though the government might continue to hold 51 per cent in LIC, there was the question of whether the guarantee would continue. One way out could be retaining the sovereign guarantee on policies already issued and discontinuing it for new policies.

If this provision has to be removed, the LIC Act has to be amended in Parliament. While there earlier were talks of amendment of the LIC Act and removal of the guarantee, a Bill was not tabled fearing a public backlash.

Earlier reports by the insurance regulator and accounting firms said listing LIC would create a level playing field in the industry. But before LIC hits the market with an initial public offering , the government would be required to recapitalise the entity.