)

The new regime for related party transactions is aimed at bringing more transparency and accountability to companies dealing with people and entities close to them. The small shareholder feels empowered but an all-encompassing definition, onerous disclosure and approval mandates have unnerved the industry. Recently, the shareholders of JSW Steel and JSW Energy approved a proposal by their respective companies to pay JSW Investments, a company fully owned by the promoter's wife, Sangita Jindal, an annual profit-linked fee for the promotion of the JSW brand.

India's state-owned explorer, Oil and Natural Gas Corporation (ONGC) uses its balance sheet to help related entities, namely the downstream refining firms to subsidise the consumers. In the last financial year, such payments crossed Rs 56,000 crore.

Another contentious area is the royalty paid by Indian subsidiaries of multinationals. Such transactions would need more approvals and therefore come under greater scrutiny.

In a June report titled 'Less is more', Institutional Investor Advisory Services, a proxy advisory firm, wrote, "The revised Clause 49 of the Listing Agreement and in some instances the Companies Act, prohibits controlling shareholders from voting on related party transactions, while allowing public shareholders to vote. This makes their vote far more valuable. This means public shareholders can now impact the outcome by vetoing transactions that they believe are unfair."

According to a definition given by the Securities and Exchange Board of India (Sebi), "a related party transaction is a transfer of resources, services or obligations between a company and a related party, regardless of whether a price is charged".

A 'related party' is a person or entity that is related to the company. "Parties are considered to be related if one party has the ability to control the other party or exercise significant influence over the other party, directly or indirectly, in making financial and/or operating decisions."

Thus, the definition of related party is wider than ever. It also includes entities related to a company if they are members of the same group, if one entity is an associate or joint venture of the other and if both entities are joint ventures of the same third party.

Under the new rules, Sebi requires that all existing 'material' related party contracts or arrangements as on the date of the circular which are likely to continue beyond March 31, 2015, to be placed for approval of the shareholders in the first general meeting subsequent to October 1, 2014.

Consultants said key challenges for companies include identifying related parties who fall under the new definition, updating and maintaining the database of such persons or entities. Companies also need to identify what amounts to ordinary course of business in relation to the company and such person or entity. The calculation of arm's length pricing for such transactions also assumes significance.

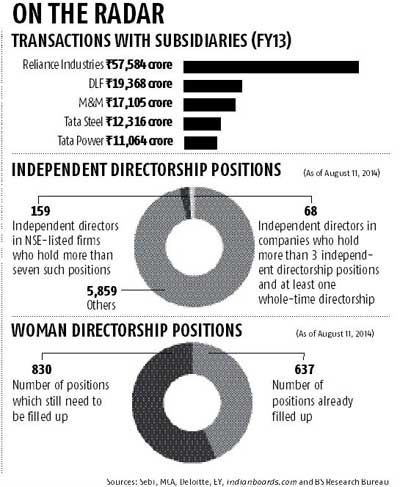

Reliance Industries (Rs 57,584 crore), DLF (Rs 19,368 crore) M&M (Rs 17,105 crore) and Tata Steel (Rs 12,316 crore) topped deals with arms. An independent director said MNCs earning huge royalty from their India-listed arms may delist Indian arms as the new norms may scuttle these payments. "If we go on pushing at it in a one-sided way, the consequences may be manifold, including delisting of MNCs. Is that what we want?" he asked.

|

CLEANER BOARDS, VIGILANT COMMITTEES, A BETTER CORPORATE INDIA The Companies Act, 2013, enacted on August 30, 2013, the rules pertaining to corporate governance notified on March 27, and the amendments to Clause 49 of the listing agreement made by Sebi on April 17, which comes into effect in October, have substantially increased the compliance pressure on companies: |

|

KEY AREAS Board of directors and its committees

|