"Aurobindo Pharma: Nod for niche drugs, strong pipeline to push earnings")

Aurobindo Pharma has been in the news and for good reasons. The most recent has been the receipt of an approval for a complex injectable product launch in the US. The approval of anti-bacterial injection, Ertapenem, provides a significant opportunity with limited competition.

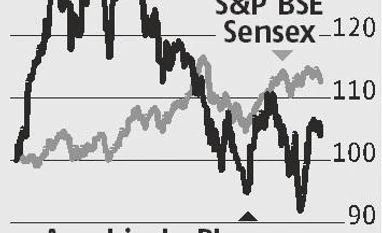

The approval has also boosted confidence in the company’s injectables portfolio and its US business. Concerns over pricing pressure in the US and FDA inspections at its various manufacturing units had pushed down its stock to 52-week lows in early June. With FDA clearance to its Unit-IV (manufactures injectables) and product approval from its penem injectables facility, Aurobindo’s prospects are looking better, say analysts.

The approved product (Ertapenem) is the generic version of Merck’s $387 million per annum brand. Assuming 60 per cent price erosion and 25 per cent market share, it could be $45-50 million revenue opportunity for Aurobindo in FY19, estimate analysts. Being a limited-competition complex product, its contribution to top line and profits will sustain for a longer period. With plans for three more penem launches, the Street is hopeful on Aurobindo.

Analysts at Elara Capital say Ertapenem approval gives comfort to Aurobindo’s ability to grow its US business in FY19, despite the high base. The clearance for Unit-IV should bolster new injectables launches and improve product supplies from the second half of FY19, add analysts.

The approval has also boosted confidence in the company’s injectables portfolio and its US business. Concerns over pricing pressure in the US and FDA inspections at its various manufacturing units had pushed down its stock to 52-week lows in early June. With FDA clearance to its Unit-IV (manufactures injectables) and product approval from its penem injectables facility, Aurobindo’s prospects are looking better, say analysts.

The approved product (Ertapenem) is the generic version of Merck’s $387 million per annum brand. Assuming 60 per cent price erosion and 25 per cent market share, it could be $45-50 million revenue opportunity for Aurobindo in FY19, estimate analysts. Being a limited-competition complex product, its contribution to top line and profits will sustain for a longer period. With plans for three more penem launches, the Street is hopeful on Aurobindo.

Analysts at Elara Capital say Ertapenem approval gives comfort to Aurobindo’s ability to grow its US business in FY19, despite the high base. The clearance for Unit-IV should bolster new injectables launches and improve product supplies from the second half of FY19, add analysts.

It is not only injectables, but other limited-competition product opportunities such as anti-hypertension ToprolXl generics, cholesterol-control Welchol generics and more from its pipeline are keeping analysts positive on Aurobindo’s US prospects. The rising basket of niche specialty products is also a positive for margins. Aurobindo, which changed its product mix to high-margin formulation sales (82 per cent of overall in FY18 from 56 per cent in FY13), saw its margins improve to 23 per cent in FY18, from 15 per cent in FY13. So, expect profitability to improve further.

Reliance Securities expects Aurobindo’s US business to clock 11 per cent compounded growth over FY18-20. While US (over 40 per cent of revenue) prospects are improving, the European business is not far behind. Europe, which contributes more than a fourth to its revenue, is also seeing a margin improvement. While all these should enhance Aurobindo’s earnings, a weak rupee will only add to its kitty.

Reliance Securities expects Aurobindo’s US business to clock 11 per cent compounded growth over FY18-20. While US (over 40 per cent of revenue) prospects are improving, the European business is not far behind. Europe, which contributes more than a fourth to its revenue, is also seeing a margin improvement. While all these should enhance Aurobindo’s earnings, a weak rupee will only add to its kitty.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in