"Auto stocks: Rising cost of ownership to impact volumes and margins")

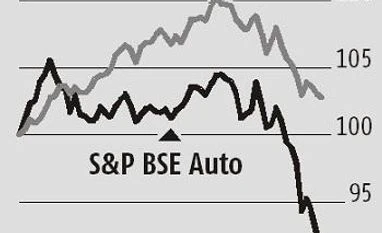

Led by two-wheeler stocks that have lost up to 5.3 per cent, the BSE Auto Index was among the highest sectoral losers, shedding 2.3 per cent in trade on Friday. Including Friday, the index has dropped over 20 per cent since the start of the year as compared to gains of 6 per cent for the benchmark Sensex.

There are multiple headwinds plaguing firms in this space. The biggest concern for the auto sector is the decline in volumes, on the back of higher product prices and running costs. Joseph George and Suraj Chheda of IIFL indicated in a report earlier this month that total ownership cost of passenger vehicles and two-wheelers was up 6-7 per cent year-on-year, primarily driven by a sharp rise in fuel cost.

Second, after the Supreme Court directive making long-term third-party insurance mandatory, upfront costs of vehicles has risen. Third, with costs for auto financiers rising, analysts expect auto loans to become more expensive, adding to the cost burden. Of these, the rise in fuel costs is the single-biggest deal breaker. Petrol and diesel prices have risen by a sharp 16-25 per cent since the start of the year, which could cause delay in new purchases.

While analysts have not yet downgraded their volume forecasts, growth is expected to slow down in the second half of the current fiscal, if costs keep spiralling.

The other worry is rising raw material costs that will impact profitability. This will impact firms especially if volumes soften, and passing on raw material costs might lead to a loss in market share. Steel and aluminium prices are on the uptick, gaining up to 16 per cent over the last year. The rupee depreciation is compounding the problem.

While there are multiple concerns in the sector, Bharat Gianani of Sharekhan says the correction in the auto space can be used to buy stocks of auto firms with leadership position and strong financial muscle. Companies such as Maruti and M&M will be able to pass on cost escalations to consumers and protect margins.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in