"Can Bajaj Auto walk the talk?")

The June numbers don't seem very encouraging either. Bajaj Auto's motorcycles sales are up 10 per cent year-on-year, while exports are up 16 per cent. Since motorcycles have formed over 70-75 per cent of total exports, this suggests growth in domestic volumes is in single digit. Analysts peg Bajaj Auto's domestic sales at 175,243 versus TVS's 176,783 for June.

The numbers are alarming, though the company insists it is still very much in control of its empire. S Ravikumar, president (business development & assurance), Bajaj Auto, describes the fall in rankings as "irrelevant, since the company only makes bikes, wherein we are the world Number 1 in profitability. Please compare not just sales but also margins and market caps."

Given that Hero MotoCorp, Honda and TVS manufacture motorcycles and scooters (the segment Bajaj exited in 2009), Ravikumar is right - but only to an extent. Data shows that while volume and market share trends in the motorcycle segment for Bajaj Auto have seen some reversal of late, the company has lost significant share in the segment over a long period.

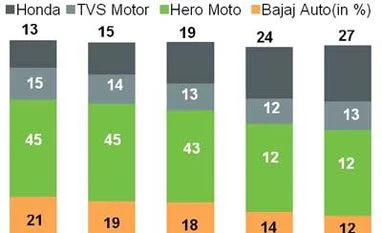

Bajaj Auto's market share in the domestic two-wheeler segment has fallen from 23 per cent in 2007-08 to 12 per cent in 2014-15, says a Motilal Oswal Securities report. The key reasons for the slide are: lack of presence in the fast-growing scooter segment; a plethora of variants under its Discover brand of motorcycles that led to confusion in the mind of consumers and, consequently, to the fall in Discover sales; and inability to break ice in the entry segment. With scooters gaining market share at the expense of the 100cc executive segment (in which Discover operates) and with Honda's entry into this segment, the impact on Bajaj Auto has been pronounced, say analysts.

The fightback

The company, however, is fighting back. Led by the re-launch of the CT100 model and the introduction of the Platina electric start variant, Bajaj Auto's market share in the economy segment has nearly doubled from 21 per cent in January to 40 per cent in April.

In the premium segment, the company has launched four variants of the Pulsar recently and more launches are planned in 2015-16. This should help, but analysts are cautious about the success of the CT100 as the company's past launches have shown weakness after the anticipation of the launch. Goldman Sachs analysts say, "The recent launches of new variants of Pulsar have not resulted in any meaningful rise in Pulsar family volumes yet."

Contesting this scepticism, Ravikumar says, "It's not true of the new launches since January of the Pulsar, Platina and CT. And it's not true of the new three-wheelers that we launched last year, which drove our share up from 50 per cent to 55 per cent".

There is no denying, however, that there still remains a question mark over the Discover's success. Domestic volumes of the Discover have been gradually declining. From a high of over 130,000 in October 2012, they were close to 25,000 in April this year. After the launch of the Discover 100M in September 2013, there was a spike in volumes for a few months, but those haven't sustained.

Motilal Oswal, in a report, said, "Rajiv Bajaj (managing director of Bajaj Auto) admitted the company made an error of judgment in the line extension of the brand positioning - from a 'fun to ride bike' to also mileage focus, creating confusion in consumers' minds as to what the brand Discover stood for. It also stretched the line extension too far with too many variants."

Bajaj Auto is trying to sort out the positioning problem. Motilal Oswal analysts say, "Discover's revival plan targets the doubling of volumes to 40,000-50,000 per month in the second half of 2015-16. There is no problem with the Discover as a product. The brand is also strong. However, the positioning needs to be sorted out."

Prayesh Jain of IIFL adds that Bajaj Auto is getting into new brands beyond the Discover and Pulsar. "When you lose a brand or market share, it's not easy to get it back," he says. "But Bajaj Auto is a well-known company. Pulsar is the number 1 brand in the premium category. So, it should not be very difficult for Bajaj Auto (to get back), though it will not be easy either."

Many say exports of both two- and three-wheelers, which have been impacted in the last 15 months, also hold the key to Bajaj's fortunes. Exports currently account for half of the company's revenues and command Ebidta (earnings before income depreciation taxation and amortisation) margins of over 20 per cent. Cumulatively, exports are up 7.9 per cent in the first quarter of 2015-16.

However, analysts are not yet building in high growth rates as seen in the previous year. Most estimates indicate that growth will remain in single digit for 2015-16. Jain of IIFL says, "Bajaj Auto majorly exports to African countries, Bangladesh and Sri Lanka. Nigeria went through tough times due to the drop in oil prices. But now it is showing stability. Egypt should also do well."

What Bajaj Auto can be happy about is its profit margin. None of its competitors come close to that. Its Ebidta margins have ranged 18-20.5 per cent in the last few years, and it aims to maintain profitability. Despite a fall in market share, Bajaj Auto's share in the profit pool (for only two-wheelers) is a third of industry's Ebidta, say Motilal Oswal analysts.

But will this last, given the rising volumes of entry-level motorcycles like Platina and CT100, which typically command low margins? While low input costs and operating leverage could help, some analysts are sceptical. Analysts at Goldman Sachs say that the CT100, along with Platina, now accounts for 50 per cent of Bajaj Auto's domestic motorcycle volumes and the quality of the domestic motorcycle mix has slipped considerably.

The company, though, says the June quarter result will be the best ever for the two-wheeler maker. Let's see if this time around, Bajaj Auto lives up to the prediction.