"Dealing with debt: DLF building on debt-free ambition")

At a time when several firms are facing insolvency, some have been able to restructure their debt. In the second of a 4-part series, Business Standard looks at the realty major

Late last month, DLF’s board of directors approved the sale of a 33.34 per cent stake in DLF Cyber City Developers (DCCDL) to an affiliate of Singapore’s sovereign wealth fund GIC for a total of Rs 8,900 crore. DCCDL would pay promoters K P Singh and family Rs 3,000 crore for buying back preference share. Proceeds from the GIC deal would also flow back to promoters who would then invest Rs 11,900 crore as equity in DLF.

With the fruition of this deal, the country’s biggest real estate firm finally managed to get back on the growth track, which would see it cutting down its Rs 26,000-crore debt by almost half. DLF has about 30 million square feet of commercial area, with an annual rent of about Rs 2,700 crore, and, out of that, DCCDL holds about 22 million square feet.

According to sources close to the company, a planned approach to selling assets is helping DLF reduce debt and also emerge as a much stronger player. This gives it an upper hand over its competitors, especially at a time when others like Jaiprakash and Amrapali are facing insolvency.

ALSO READ: Part I: Dealing with debt: GMR builds cash pile on divestment plank

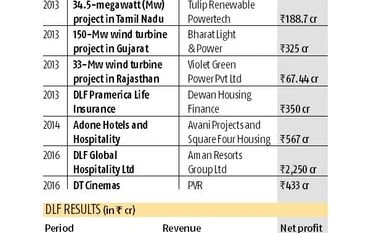

“Over the years, the company has been selling its non-core businesses like insurance, hotels, wind energy businesses to reduce debt. Going forward, the promoters will be infusing a substantial part of their proceeds into DLF to reduce the company’s debt, which will happen once GIC pays the money to the DLF promoters for the 33 per cent stake in DCCDL,” the person said. Seven divestments since 2013 have brought Rs 4,181 crore into the company.

The DCCDL-GIC deal is set to be completed by November after all the regulatory approvals, including that of the Competition Commission of India.

“In such a scenario, developers, with leased assets or even undeveloped, licensed land parcels, are willing to sell off equity or offload such land holdings to generate positive cash flows and reduce their current debt burden. On the whole, all attempts are being made by developers to reduce their debt burden, while they are selectively starting new projects to ensure cash flows in the future as well,” said Ramesh Nair, chief executive officer and country head, JLL India.

Beyond the GIC deal, the developer is also relying on its vast inventory of residential properties worth Rs 15,000 crore to reduce debt. It would start selling these properties over the next few months.

“In the past four years, we have fulfilled all our commitments and delivered over 14.5 million square feet per annum. We now have an inventory of ready-to-unlock and occupy stock of Rs 15,000 crore. Not selling residential properties for the past few months was a legal requirement for all builders across the country. It was a conscience decision to first register with real estate regulatory authority (RERA),” said Rajeev Talwar, chief executive officer, DLF Limited.

The company hopes that once the beleaguered residential segment settles down over the next few quarters, it would be able to sell its ready-to-move-in properties at a premium. If things move as envisaged, the company hopes to be debt-free in the next two to three years.

The company is also completing its other commercial projects, few of which it believes would be sure-shot game-changers.

“Expansion of the commercial portfolio is under process and approximately 4.5 million square feet is being added to the portfolio. It will open the doors to Chanakya Mall in the coming festive season. The company will be in the growth stage in the next few quarters. The unlocking of value of the finished inventory will help the company in medium and long run,” sources close to the company said.

Part III: Future group -- De-merging infra for profitable growth

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in