"Falling iron ore prices a boost for steel producers")

Global iron ore prices have been on a continuous decline since the highs of $95 a tonne in February this year to about $56 now, primarily due to slowdown in Chinese demand. Analysts at IIFL highlight that iron ore inventory levels at Chinese ports have risen by 40 per cent over past one year and 15 per cent year-to-date in 2017. The Chinese government had directed steel producers to decrease the metal’s output in a bid to reduce pollution. Thus, while iron ore imports were 8.5 per cent higher during January-April, steel production was comparatively much lower at 4.8 per cent.

All this has led to iron ore prices tumbling, which analysts at IIFL estimate to hover between $50-65 in the near-term. Prices, however, could get some support if some of the iron ore production is cut.

The decline in iron ore prices has not been good news for India’s largest iron ore producer NMDC, which has also seen its stock price correct by almost 32 per cent from the highs of Rs 152.50 in March to Rs 104 now. The limited downside in iron ore prices from here on, though, should cushion further decline for NMDC. Analysts say NMDC’s FY18 volumes and earning may see an impact, which, though, is now factored in the stock. In fact, analysts at Motilal Oswal, in their recent note, have maintained ‘buy’ rating on NMDC looking at its high-quality iron ore and low-cost operations, as they feel valuations, too, are attractive now.

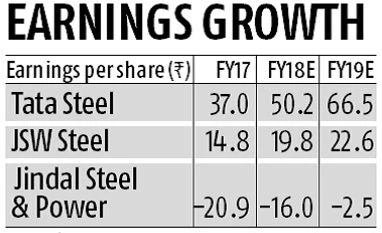

Analysts at Motilal Oswal also see demand-supply equation for steel improving as they forecast steel demand to grow 7.3 per cent CAGR over the next 10 years. The recent investments in creating new capacities will only help meet demand for the next three years, they said. Looking at the stretched balance sheet of most private steel producers and poor execution track record of public sector players, analysts believe only JSW Steel and Tata Steel have balance sheets to support investments in new capacity and hence these stocks remain their top picks.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in