"From HUL to Maruti Suzuki, India arms now mean more to MNCs: Here's why")

The Indian subsidiaries of global multinationals like Unilever, Suzuki, Siemens, Colgate-Palmolive and ABB are running at double the pace of their global parents in terms of market value.

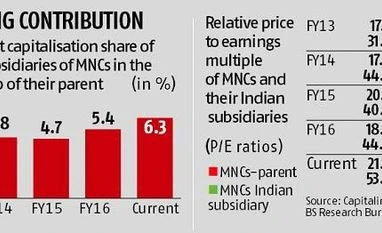

Multinational companies’ Indian arms listed on Dalal Street now account for 6.3 per cent of their global parents’ market capitalisation, against 3.1 per cent at the beginning of 2013.

Maruti Suzuki and Hindustan Unilever are the biggest contributors to this surge. At its current stock price, Maruti’s market capitalisation is nearly 50 per cent more than its Japanese parent Suzuki Motor’s, while HUL’s market cap now is 28 per cent of Unilever’s.

Over the past five years, the combined market capitalisation of 52 Indian subsidiaries studied for this analysis has risen 120 per cent in dollar terms, compared with an increase of 10 per cent in the combined market capitalisation of their parents. As a result, Indian subsidiaries are now trading at a 150 per cent premium to their parents on the basis of price-to-earnings multiples, against 80 per cent at the start of the current rally in 2013.

Analysts attribute this to the fact that the rally seen by Dalal Street has been much more powerful than other major markets. “The stock rally in India has been much stronger than in most developed markets. This has greatly benefited MNCs, most of which are leaders in consumer segments, where investors’ interest has been the greatest,” says Dhananjay Sinha, head of research, Emkay Global Financial Services.

The analysis is based on the annual revenue and profit of MNCs’ arms listed in India and the global parents. The market capitalisation data taken for the analysis are from the end of the period for each financial year. Data for the current year data are on a trailing 12-months basis. For MNCs with more than one listed subsidiary in India, the numbers have been consolidated. All numbers are in US dollar terms.

Even as Indian subsidiaries have raised their financial contribution to their parents’ coffers during the period under review, the proportionate rise in revenues and profits has been much less than the rally in stock prices. Their revenue contribution has risen by 40 basis points, while net profit contribution is up 60 basis points. Besides, it should be noted that the momentum is now waning, with growth reviving in the developed world.

The listed Indian subsidiaries of 47 global multinationals in the Business Standard sample now account for 2.4 per cent of their parents’ global revenues, up from two per cent five years ago. During the same period, Indian subsidiaries’ contribution to their parents’ profits increased to 2.4 per cent from 1.8 per cent in 2013.

According to experts, this could be due to a faster rate of economic growth in India, besides the impact of currency movements. “Developed economies took much longer than India to come out of the recession triggered by the Lehman crisis. Besides, the Indian economy never stopped growing, even at the depth of the economic slowdown, unlike many developed economies that are the home markets for MNCs,” says G Chokkalingam, founder & MD, Equinomics Research & Advisory.

The Indian subsidiaries’ better financial performance than their parents in the past five years is also evident in revenues. The combined global revenues of MNCs has been down 6.9 per cent since 2012-13, compared to a 12.6 per cent rise in Indian subsidiaries’ revenues in dollar terms during the same period. The Indian subsidiaries’ combined revenues, however, would be down 0.3 per cent during this period, if Maruti Suzuki were to be removed from the sample.

The combined net profit of global MNCs is down 4.4 per cent during the period, against 30.6 per cent growth in the combined net profit of Indian subsidiaries. The profit growth for Indian arms, however, drops to 4.9 per cent if we exclude Maruti Suzuki, and to 1.1 per cent if Hindustan Unilever is excluded from the sample.

Going forward, however, Indian subsidiaries will have to grow faster to stay ahead of parents, as the recovery in the developed countries is expected to be quicker than India, where growth has been hit by demonetisation and the rollout of the goods and services tax (GST) in recent times. “Corporate earnings are likely to grow faster (in constant currency terms) in developed countries than India, where MNCs are now reporting low single-digit growth in volumes and revenues,” says Chokkalingam.

The combined global revenues of MNCs in 2017-18 is up 1.7 per cent on a trailing 12-month basis, against 1.4 per cent growth reported by their Indian subsidiaries during the period. Excluding Maruti and Hindustan Unilever, however, the Indian subsidiaries’ combined revenue would be down 4.3 per cent in the current financial year.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in