"Growth concerns resurface for Sun Pharma after disappointing second quarter")

Shares of Sun Pharmaceuticals Industries lost a little more than seven per cent after the company reported a lower-than-expected performance for the September quarter. The results were declared after market hours on Tuesday.

Market sentiment had earlier improved on Sun’s business growth in the US having picked up after clearance of its Halol (Gujarat) plant by that country’s regulatory agency for the segment, launch of its speciality portfolio and supported by domestic sales growth. While the miss in performance in the quarter (the second one or Q2 in the financial year) was largely led by one-offs, sentiment on the Street was bound to be hit.

For, after around half a dozen quarters of decline in sales and profit, Sun had reported double-digit growth in the June quarter. The Street was looking for a 13-14 per cent increase in net profit during Q2.

Now, however, with the performance below estimates, even after adjusting for the one-offs, and a discouraging outlook, the growth concerns have resurfaced. The adjusted net profit was Rs 9.9 billion, lower than the Bloomberg consensus estimate of Rs 10.45 billion.

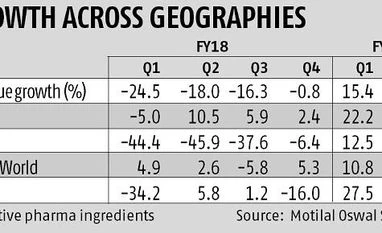

Weaker show

To the Street’s disappointment, sale of branded formulations in India for Q2 (27 per cent of the total), at Rs 18.6 billion, declined by 16 per cent. Mainly due to a planned one-time inventory reduction in the supply chain, coupled with the higher base of Q2 last year. Analysts, factoring in last year’s high base due to re-stocking after implementation of the goods and services tax (GST), were still expecting this segment to grow about 8 per cent, year on year.

The decline on account of inventory reduction has surprised them, as a large amount of de-stocking (due to GST) had happened only 12 months before, said one. Due to this inventory adjustment, those at IIFL feel, the next few quarters will show muted growth for Sun’s India business. The management, though, says it expects normalised growth in the low mid-teens (year on year) for its India formulation sales in FY19 (which grew only one per cent in the financial year’s first half). Surjit Pal at brokerage Prabhudas Lilladher says that assuming a 13 per cent growth for 2018-19, India formulation sales need to grow 25 per cent in the second half, which seems very unlikely.

US did well

Positive news came from the company’s US business, 35 per cent of consolidated revenue. It reported sales of $342 million, an increase of 11 per cent over Q2 of last year. In rupee terms, the number would be more, given the dollar’s strengthening. The company had already commercialised carcinoma drug Odomzo and psoriasis drug Ilumya. It recently commercialised Yonsa, an anti-cancer drug, and will be soon launching Xelpros and Cequa, both for ophthalmology. Sun focusing on its specialities portfolio but has indicated rising costs (in the initial period) as it launches new products; the latter will see ramp-up only gradually. This has added to analyst concerns. Those at Edelweiss Securities say the near-term challenges and investments in the speciality business eclipse the medium-term outlook, despite Sun’s business being among the best in the segment.

Further, while the US subsidiary, Taro, surprised with net profit rising 19 per cent over a year before (down seven per cent sequentially), this was supported by $4 million related to settlement of a patent infringement and lower foreign exchange losses of $6 million as against $32.6 mn in Q2 of FY18. Operating earnings actually fell 10 per cent over the year. Hence, analysts expect the challenges for Taro to continue.

Sun also saw flat sales growth in emerging markets at $195 mn for Q2; those in the rest of the world fell two per cent. So, analysts say it has reported all-round weak performance across the regions.

Sun has also accounted for Rs 12.1 billion under exceptional items, relating to the Modafinil anti-trust litigation in the US. This was unexpected, as some provisioning for this was done earlier. The company has indicated there will be no more provisioning on this account but concern on near-term growth in both the US and India (the majority revenue contributors) have led to some pruning in earnings estimates. While Edelweiss has cut its FY19 and FY20 estimates by five per cent each, Motilal Oswal Securities has cut these by six and three per cent, respectively.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in