"HDFC Bank Q4 net profit growth slowest in 10 yrs")

This was the third quarter in a row when the year-on-year rise in its three-month net profit was below 30 per cent. The country’s second largest private sector lender had been growing its quarterly net profit at over 30 per cent for more than a decade till the first quarter of FY14.

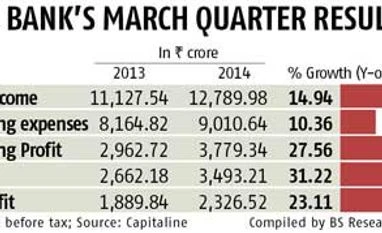

The performance is, however, healthy in the overall context of slowing economic growth and particularly the rise in tax rate. The bank’s effective tax rate was higher at 33.4 per cent in January-March compared to 29 per cent in the year-ago quarter — tax outgo thus jumped 51 per cent to Rs 1,167 crore.

For 2013-14, net profit was up 26 per cent to Rs 8,478 crore. The effective tax rate for the year was 33.6 per cent, against 31 per cent in 2012-13.

An improved net interest margin (NIM), lower provisioning and tight cost control aided the quarter's earnings growth. While asset quality remained resilient to macro pressures, there were weak areas in the results, thanks to slowing economic growth. Growth in fees and commissions moderated from 11-13 per cent in the past three quarters to 10 per cent in the March 2014 quarter. Net interest income growth too has moderated from 21-32 per cent since the June 2013 quarter to 15-16 per cent since the September 2013 one.

“We have been saying that we aim to grow a little faster than the system, maintain our margin in a certain range and manage the growth without compromising our asset quality. We have delivered on all these parameters,” said Paresh Sukthankar, deputy managing director, in his post-earnings comments.

Net interest income, the difference between interest income and expense, was up 15.3 per cent over a year at Rs 4,953 crore during the March quarter. NIMs were down 10 basis points over a year but improved sequentially by 20 basis points, to 4.4 per cent aided by growth in the low-cost deposit base. HDFC Bank has been maintaining a forecast of a margin in the range of 3.9-4.4 per cent.

Other income grew 11 per cent over a year, to Rs 2,001 crore. Operating expenses were up only 1.2 per cent, improving the cost to income ratio to 45.7 per cent, compared to 51.4 per cent in the year-ago quarter. While cost optimisation is a positive, further improvement in this appears difficult, say analysts.

Improved asset quality allowed the bank to cut its provisioning in the quarter to Rs 286 crore from Rs 300.5 crore a year earlier. The gross non-performing asset (NPA) ratio was 0.98 per cent of the total; the net NPA ratio was 0.3 per cent at the end of March.

“Our historical average for gross NPA has been 1.2-1.3 per cent. So, not only have we done better than the system but have also reduced it below our own average. On the wholesale side, we have largely avoided some of the projects that got stuck or highly leveraged groups. Our diversified loan book and cautious approach helped us,” said Sukthankar.

The total of restructured loans (including applications under process) was 0.2 per cent of gross advances.

Capital adequacy

The bank's advances were up 26.4 per cent over a year to Rs 303,000 crore, driven by growth in corporate loans, which rose 37 per cent. Retail loans were up 10 per cent. The domestic loan mix between retail and wholesale categories was 53:47 at the end of March.

“The major part of the growth in loan book this quarter has come from the wholesale side. We have seen demand for working capital but not any meaningful rise in greenfield capex (led-loan demand). Going forward, we see equal growth opportunities in both wholesale and retail loans,” said Sukthankar. Total deposits were Rs 367,337 crore, up 24 per cent over a year. The share of low-cost current account and savings account deposits was 44.8 per cent of total deposits.

Loan and deposit growth, however, were boosted by a one-time increase in foreign currency non-resident Indian deposits, swapped with the Reserve Bank of India under the special window opened for this in the December 2013 quarter, and the related foreign currency loans. Adjusting for this, the loan book and deposits grew 21.8 per cent and 16.9 per cent, respectively. While loan growth was in line with analysts' expectations, deposit growth was lower than the estimate of 19 per cent.

HDFC Bank closed the year with a capital adequacy ratio of 16.1 per cent (Tier-I was 11.8 per cent) as in the Basel-III rules.

Analysts continue to be positive on the scrip. “HDFC Bank continued its trend of delivering consistent earnings and asset quality performance quarter after quarter. From a long-term perspective, we believe it is a decent investment. Hence, we recommend a 'buy' rating on the stock,” said Vaibhav Agrawal, vice-president for research, banking, at Angel Broking.