"High base not growth deterrent for Cadila, high launches may drive earning")

Cadila Healthcare, unlike many of its peers, seems to be a bright spot in the pharma space. The company, which has been buzzing with news on approvals of drug launches, announced on Wednesday the USFDA’s approval for its Ahmedabad-based SEZ facility. The unit, which manufactures oncology injectables for regulated markets, was inspected from 28 May to June 5 and has not received observations by the drug regulator.

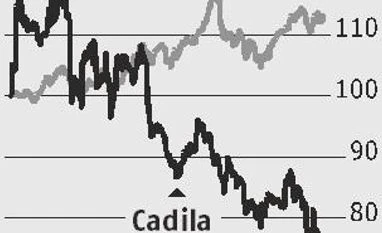

With this, Cadila, which resolved the FDA warning letter for its Moriaya plant last year, has no regulatory overhang. In fact, the strong product pipeline for the US market and faster pace of approvals after the FDA resolution, bode well for growth. The stock, which has been trending down due to weak sentiment towards the pharma sector, could provide a good opportunity for investors at current valuations, said analysts.

Consider this, Cadila posted a strong 54 per cent year-on-year increase in net profit during the March quarter, led by 67 per cent growth in the US business. This surge in profit was also helped by exclusivity sales of generic, Lailda (ulcerative colitis treatment) and due to March being a seasonally strong quarter for generic Tamiflu (flue treatment). Because of this, there are fears that as the exclusivity sales period has ended, Lailda’s contribution may decline, leading to pressure on US sales. However, analysts differ.

A key reason for the confidence is Cadila’s 144 pending approvals in the US and 77 approvals received (including eight tentative) in FY18, of which only 20 had been launched. Analysts believe that such a strong pipeline will help support growth in FY19 too. Praful Bohra at Equirus Research says that high-value products like Toprol, the generic of anti-hypertensive, and the launch of Asacol HD, its own generics of anti-inflammatory — can provide triggers.

With stock valuations at a reasonable 17 times one-year forward earnings, there is some cushion on the downside too.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in