"Hindustan Zinc well placed with rising volumes, supply situation")

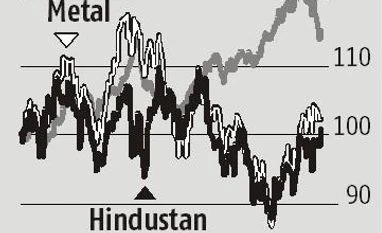

Though the broader markets have been under pressure, Hindustan Zinc continues to gain and has bounced back 13.8 per cent from its July lows. While trade war concerns have led to volatility in base metal prices, what offers comfort is the outlook for zinc given the supply shortages.

Further, while it posted softer volumes in the June quarter, there has been a recovery and analysts expect a better second half. The firm is on track to achieve a 1.2 million tonnes per annum (MTPA) run-rate by the end of FY19, as compared to 0.94 MTPA in FY18. It is further planning to ramp up volumes to 1.5 MTPA. Thus, improving volume outlook and zinc supply deficit should help support its stock prices.

Zinc prices on the London Metal Exchange have remained volatile. Analysts at Kotak Securities say the zinc market is expected to remain in a deficit this year and foresee Hindustan Zinc to benefit from the favorable zinc environment, resulting in cumulative free cash flow of Rs 210 billion by the end of FY20.

Global zinc consumption is expected to grow 2.5 per cent to 14.8 MT in 2018, while mine supply will remain at 13.7MT, say analysts.

On volume front, August saw lead production volumes shoot up 35 per cent year-on-year (48 per cent month-on-month) to 18,100 tonnes.

Volumes have improved 28 per cent month-on-month to 58,500 tonnes as the underground transition at Rampur Agucha mines remains in progress. Analysts at Edelweiss expect mined metal production to revive to 80,000 tonnes in September.

The firm continues to be one of the lowest cost producers globally. What helps it further is its presence in the lower end of the cost curve globally (backed by high grade captive mines), a diversified revenue stream with increasing contribution from silver, and a strong balance sheet.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in