"How effective is PNB's war room?")

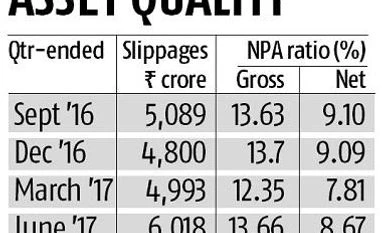

With a gross non-performing assets (NPA) ratio at upwards of 13 per cent, investors are unlikely to believe that the firefighting by Punjab National Bank (PNB) is yielding the desired results. However, the lender’s September quarter (Q2) performance reveals that the war room created about a year back to fight against bad loan accretion is perhaps showing some results.

The biggest sign of improvement was that slippages or accretion of bad loans in Q2 reduced to Rs 3,517 crore — the lowest in recent times. This helped the gross NPA ratio dip to 13.31 per cent, from 13.63 per cent a year ago.

The net NPA ratio, too, softened to 8.44 per cent, from 9.1 per cent in the year-ago period. But, provisioning costs in the quarter were up 24.5 per cent year-on-year (y-o-y) at Rs 2,718 crore.

All these indicate that the asset quality should perhaps stabilise in the coming quarters, and normalcy could be at least 18-24 months away.

An improvement in income statement and balance sheet has buoyed PNB’s financials in Q2. Its net interest income at Rs 4,015 crore (up 3.5 per cent y-o-y) and net profit at Rs 561 crore (up two per cent y-o-y) have bettered the Street’s expectations. A 16 per cent y-o-y increase in the bank’s operating profit at Rs 3,279 crore indicates that much of the Q2 performance has drawn support from its core operations.

Net interest margin, a profitability indicator, stood at 2.64 per cent in Q2, lower than the year-ago level of 2.86 per cent, indicating that a higher share of low-cost loans is eating into the bank’s profitability.

Ideally, PNB’s next battle should be towards reducing the sticky 13 per cent gross NPA ratio.

What is a positive is that if private banks have just begun to recognise certain telecom and iron and steel loan accounts as NPAs after the Reserve Bank of India scrutiny, with PNB having already recognised these accounts as bad, provides comfort that much of the stress recognition is behind. The game is now on to resolution, which is unpredictable, patchy, and slow for the sector, and could reflect on quarterly performances of the banks.

PNB’s investment in non-core assets such as PNB Housing, PNB Metlife, SIDBI and UTI, however, should help it in times of need.

According to Antique Stock Broking, these non-core assets represent 42 per cent of PNB’s market capitalisation.

“Non-core assets are our hidden strength and we will divest these investments depending on market condition,” Sunil Mehta, managing director and CEO, PNB, had said.

If PNB plays the divestment game right, that should help absorb loan losses and augment its capital. A benign valuation of 1.2 times its FY19 estimated price-to-book value also adds sheen to the PNB stock.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in