"IL&FS crisis: NBFC cash crunch to trigger real estate consolidation")

The blow up at IL&FS, which led to the domino effect of tightened scrutiny and lending at NBFCs, took a swipe at the markets last week with realty stocks sliding across the board.

This could be a sign that there may be deeper implications for the sector, especially for small players who may find it very difficult to secure working capital.

Already, the real estate sector is reeling from pressure due to subdued demand and rising costs.

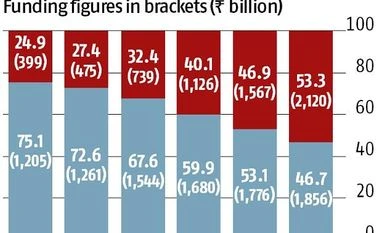

The latest problem would mean further squeeze of funds and from a segment that now accounts for a big chunk of loans. By rough estimates, non-banking finance companies (NBFCs) and housing finance companies (HFCs) have 40 per cent funding exposure to the realty sector.

According to Anil Gupta, head financial service sector ratings at ICRA, "amid liquidity crunch, refinancing for real estate developers may become difficult. Real estate projects which are at nascent stage – land acquisition and pre-launch would also face challenges in funding tie-ups. This could impact the launching of new projects in near term.”

According to Anil Gupta, head financial service sector ratings at ICRA, "amid liquidity crunch, refinancing for real estate developers may become difficult. Real estate projects which are at nascent stage – land acquisition and pre-launch would also face challenges in funding tie-ups. This could impact the launching of new projects in near term.”

But how did it get to this point? Somewhere around 2012, the real estate sector started to splutter. If it hadn't been for large NBFCs, many companies would have been left high and dry. “NBFCs essentially bailed out the real estate scene and took huge asset covers on land,” said Samir Jasuja, founder of analytics firm PropEquity. From a landscape perspective, it accelerated development of apartments. This led to markets like Gurugram, which normally had 3,000 apartments a year come up for sale, see 35,000 units being built annually.

That combined with subvention schemes with banks enabled customers to pay 10 per cent of the property value and get a bank to fund the rest. It also saw developers optimistically increase supply which is why there's a considerable supply overhang in the market.

Anuj Puri, founder of Anarock Property Consultants, said commercial real estate is doing just fine but that represents only 16 per cent of the sector. “The last five years have been hard for the residential segment but the silver lining is that sales have been more than new launches, which means new launches have rationalised and unsold inventory has come down,” Puri said, adding that with the NBFC liquidity crunch, developers could see a slowdown for construction, which in its own way will have ramifications that could impact consumer confidence. So, it is important that funding continues.

Although reports suggest that property sales have picked up a bit in the September quarter, JM Financial estimates that inventory liquidation would still take three years at the current sales pace. While it will take long for the sector to see its fortunes revive, Puri believes that there will be consolidation and that could mean new projects getting re-branded under joint ventures or new names, but not outright buys. One example is Sunteck Realty, he said, which acquired a project in Naigaon in Mumbai and sold over 1,500 units in September.

Smaller players could see turbulence if they can't acquire funding alternatives. “Medium and small size firms could face pressure to sell inventory at discounts on the back of a tight funding scenario,” said Prakash Agarwal, head of the banking, financial services and insurance (BFSI) vertical at India Ratings. “Optionally, they can tie up with larger players,” he said.

Interestingly, in the National Capital Region (NCR), over 70 per cent of the projects pending execution are fully sold out, but not delivered after the completion deadline. Hence, developers here are under maximum distress as they face buyer pressure to complete the sold units, Jasuja said.

With stricter compliance under Real Estate Regulatory Act (RERA) and high penalties payable for non-delivery or delayed deliveries, time is running out.

One developer said that the few companies which had a track record of delivering on time, had ready inventory on hold and less than 20 per cent of borrowing came from NBFCs. Hence, such players would see little impact by the squeeze in financing.

In general, analysts see DLF, Godrej Properties, Prestige Estates and Sunteck Realty as players who are likely to come out stronger. The key, of course, to it all when it comes to big-ticket buys like homes, which are long-term purchases for most, is ensuring that consumer sentiment isn’t affected to the point of saturating buyers.

With inputs from Shreepad S Aute

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in