"India Inc high on profit, low on sales growth in second quarter")

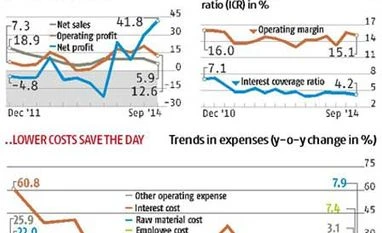

During the quarter ended September 30, the net profit (adjusted for exceptional items) of 2,432 companies (excluding banking & financial and oil & gas ones) rose 41.8 per cent on a year-on-year basis — the fastest pace in at least three years — but their net annual sales growth slumped to 5.9 per cent, slowest in five quarters.

The same set of companies had in the previous quarter reported 29.8 per cent annual net profit growth and 10.1 per cent increase in net sales, raising hope of a swift recovery in India’s growth cycle and corporate earnings. The dichotomy between top-line and bottom-line growth rates in the September quarter has tempered the growth expectation among experts and analysts.

Devang Mehta, senior vice-president & head of equity sales at Anand Rathi Financial Services, says: “The result season was mixed, with no definite trend. While top companies in export-driven sectors did well, like in earlier quarters, firms in investment and capital expenditure-related sectors (capital goods and construction & infrastructure, for example) reported poor numbers. It seems we have to wait a little longer for a full-blown economic recovery.”

The profitability was boosted by last year’s low base and lower operational cost, especially with a drop in sales & marketing expenses, finance cost and depreciation allowances. This set of companies had reported an annual decline of 21.9 per cent in net profit during the corresponding quarter of last year.

Cost moderation in the July-September period led to an improvement of 90 basis points in core operating margins (excluding other income) on a year-on-year basis to 15.1 per cent of net sales, against 14.2 per cent a year ago. The bad news was that the operating margin was down 50 basis points on a sequential basis. One basis point is one-hundredth of a percentage point.

Stability in the rupee-dollar exchange rate and the recent decline in international commodity prices are likely to aid margins in the coming quarters as well, though the net impact would get moderated by lower top-line growth. Some analysts expect a rise in competitive intensity as companies try to push volumes on the back of lower commodity prices.

In what hints at a continued slowdown in capex cycle, annual net sales growth for capital goods makers fell to 1.4 per cent from 2.9 per cent in the previous quarter. Their net profit, which grew 5.6 per cent on a year-on-year basis, showed an improvement over previous quarters. Construction & infrastructure companies, on the other hand, reported 93.4 per cent annual decline in net profit, while their net sales fell 1.1 per cent in the September quarter.

The results also indicated a moderation in consumption demand, with net profit of FMCG companies growing at the slowest pace in 12 quarters (7.8 per cent) and their net sales growth slumping to the lowest in four quarters.

Analysts expect more growth pangs for India Inc ahead as the central government cuts expenditure in the second half of the current financial year to bring its fiscal deficit down to the targeted level. "The government is likely to shave off nearly Rs 1.2 lakh crore of expenditure and subsidies between now and the end of March. That will make it tough for companies to grow their top lines during the second half of 2014-15," says Dhananjay Sinha, head of institutional equity at Emkay Global Financial Services.

The impact would be the most on companies in the construction & infrastructure and capital goods sectors, followed by those in FMCG and consumer durables ones. "A cut in subsidies will lead to a reduction in disposable income, especially in rural areas. That will force consumers to lower their expenses on staples and durables," Sinha adds.

On the brighter side, a slowdown in public expenditure might translate into lower consumer inflation and a stable rupee-dollar exchange rate, providing relief to companies on their cost side. This, coupled with a decline in international commodity prices, would help companies with the ability to maintain pricing power despite a demand slowdown.