"Infosys: Buyback won't move the needle")

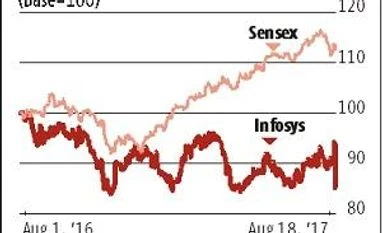

Infosys’ first-ever buyback programme of Rs 13,000 crore at a price of Rs 1,150 per share is at a whopping 24.6 per cent premium to its Friday’s closing price of Rs 923. Normally, a buyback of this nature would be welcomed by investors, given that the company has been very rigid in the past on returning cash back to shareholders and also in acquiring companies. Further, it is expected to boost the company’s return ratios following efficient use of its $6 billion (Rs 38,000 crore) cash pile.

However, despite the positives, the buyback is unlikely to move the needle much as far as investor sentiment is concerned. For one, the offer is in line with the Street expectations. Experts say the tussle between the founder-promoters and the company board, which led to the resignation of the company’s managing director (MD) & chief executive officer (CEO) on Friday, will weigh on the stock. The uncertainties could also have an impact on the company’s performance.

Ravi Menon of Elara Securities, in an August 19 report, said, “With the board of directors accepting Vishal Sikka’s resignation, we expect Infosys to lose confidence of investors as well as clients. Under Sikka, the strategy of building differentiation through Infosys-developed intellectual property and constant innovation had helped the company improve its incremental organic revenue market share (among Tier-1 India peers) to 18.3 per cent over FY16, from the low point of 9.9 per cent in FY15.”

Other analysts also point to the concerns that could emerge going ahead. “The more important issue for Infosys is the uncertainty and new issues cropping up, which will keep a lid on the stock price,” says an analyst at a domestic brokerage, referring to the possible lawsuit against the company for securities fraud by a few US-based investors. With business challenges mounting due to muted growth in key sectors such as retail and BFSI (banking, financial services and insurance), distractions for the top management will take a toll on the stock.

Another analyst, who did not want to be named, says, “Despite the management assurances, foreign investors, who were largely responsible for the sharp fall in the company’s stock on Friday, could look at alternatives (Tata Consultancy Services or TCS among others), as the new CEO search could end up being a protracted one and transformation programme will take time to bear fruit.”

All these uncertainties are also rubbing off on valuations of the Infosys’ stock . While most analysts have not yet cut their earnings estimates for the company, quite a few have lowered their ratings for the stock on Friday. These downgrades are more on account of the analysts lowering their price-to-earnings multiple (de-rating the stock), given the lack of a stable management team and the ongoing battle between the founder-promoters and the company board over corporate governance issues.

However, despite the near-term worries, analysts also do not expect the stock price to fall below the Rs 840 levels. This is because even after the Lehmann crisis, the stock has not traded below 12 times one year price-to-earnings (P/E) ratio. Given FY19 earnings per share of about Rs 70 and conservative one year forward P/E estimates of 12-13 times analysts expect the stock to find support in the Rs 840-910 zone. The stock is currently trading at 13 times its FY19 estimates.

Says an analyst, “Typically, long-only investors and some small investors do not tender but given the situation and the higher retail base, a large number will look to tender the shares, pushing down the acceptance ratio.”

Even then, most analysts are advising investors to tender the shares given the near term worries.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in