"Lanco: Fighting a grim battle")

But analysts say this isn't enough for Lanco to get out of the debt trap. Most of the company's projects are facing litigation relating to fuel supply, cost of generation and/or off-take disputes, apart from rising interest payments on its loans.

"We believe issues of cash-flow crunch are unlikely to be resolved in the near term, despite the Udupi stake sale and CDR (corporate debt restructuring) being approved, as these will only help put equity in stuck, under-construction projects. In the medium-to-long term, problems due to projects facing issues of fuel security or non-viable power purchase agreements will emerge," Emkay Research analyst Amit Golcha said in a report dated August 18. "We do not see a significant upside unless clarity emerges on fuel supply, especially for merchant/gas plants, offtake and offtake disputes, and debt reduction."

This is bad news for Lanco's investors, who were expecting the company to turn around, in line with the overall economy, owing to a stable, pro-business government at the Centre. Since January this year, the company stock has fallen 17 per cent; in the past five years, it has declined 98 per cent.

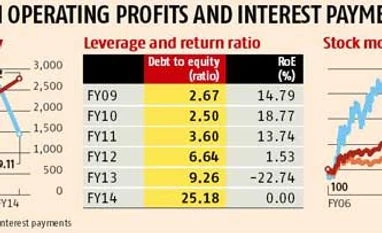

And, the company's mounting debt is eating into its cash flow. In 2013-14, the company paid interest of Rs 2,762 crore, while its operating profit stood at Rs 1,449 crore. In 2012-13, operating profit was Rs 2,665 crore, while interest payment stood at Rs 2,421 crore, showing the company's inability to generate enough money to repay its loans in recent years. In 2013-14, the company's debt-to-equity ratio was 25.18, compared with 9.26 in 2012-13; in 2012-13, its return on equity was a negative 22.74 per cent.

Issues before Lanco

In a statement in September, the company admitted it was in financial woes, and was taking steps to raise funds. Citing the micro-economic environment in the past three years, Lanco said it couldn't raise funds either through an initial public offering or a qualified institutional placement, as initially planned.

"Lanco plans to sell 3,000 Mw of assets to raise Rs 5,000 crore and reduce additional debt of Rs 15,000 crore," the company had said. It added the financial health of state government-owned electricity distributors should be improved on a priority basis so that they could pay power generation companies.

But analysts aren't enthused by these arguments. "For Lanco, we believe the issue of cash flow crunch is unlikely to be resolved in the medium term, given most projects are likely to be under stress. Cash flow from the Udupi deal and CDR will merely postpone the issue," they say.

During the quarter ended June, the production of Griffin Coal, Lanco's Australian subsidiary, hit a low of 0.61 million tonnes (mt), down 25 per cent year-on-year.

Lanco had acquired Griffin Coal for $605 million (A$750 million) in 2011.

Initially, it was planned Griffin Coal's production would be increased to five mt a year. However, since Lanco acquired the company, its production has declined 40 per cent. Since then, it has also been losing money, following depreciation and interest expenses, according to stock exchange data.

"The coal production is controlled to the extent of local market requirement," a company spokesperson said in an emailed response.

In the past, the company had said it would sell part of its stake in Griffin. But owing to low valuations, it has decided to postpone the sale. After the surge to almost Rs 15 in May this year from its all-time low of near Rs 5 in August 2013, Lanco's stock is back to below Rs 7 levels currently. In this scenario, it may not be easy to raise significant money via the equity route without sizeable equity dilution. As such, the wait for investors to expect a turnaround in Lanco's fortunes has been extended.