"Limited upside at upstream oil firms")

The oil and gas sector has been buzzing with news flow. In the latest one, the government on Thursday cleared a changed exploration and licensing policy.

It has introduced a uniform licence for all fuels (natural gas, crude oil or shale gas). Explorers (upstream entities in sector jargon) get the freedom to price petroleum products procured from hard-to-explore deep waters at market rates. Some licences for small and medium size fields have been extended and production sharing contracts for many have been extended till the economic life of such assets.

This is positive for the sector, as it removes anomalies and will accrue benefits in exploration activities but in the long run.

In the near term, it will not have much impact on companies’ earnings, say analysts.

Thus, the scrip of government-owned upstream entities such as Oil and Natural Gas Corporation (ONGC) and Oil India did not react much, closing at Rs 205.70 (up 0.3 per cent) and Rs 309.55 (up 0.06 per cent), respectively, on Thursday.

The bigger news has been the sharp rise in oil prices, from $33 levels at end-February to $40 a barrel. The stocks have gained significantly, with ONGC up six per cent and Cairn India by 21 per cent from their lows on Budget Day. Oil India has not seen much rise, due to concerns on production from maturing fields. Nevertheless, higher crude oil prices are always beneficial for producers.

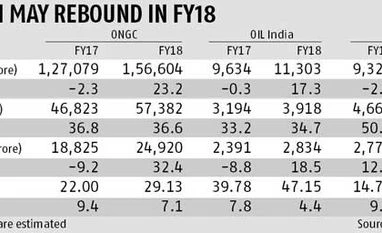

Analysts do not see oil prices rising significantly in the near to medium term. They see it averaging $45-50 in FY17, similar to the levels in FY16. It is only from FY18 that analysts expect a recovery in crude oil prices. For instance, analysts at HSBC estimate $45/60/75 a barrel in FY17/18/19, respectively. With revised cess rates, they see a three per cent rise in FY17 earnings for Cairn India, a one per cent negative impact on earnings for ONGC and the earnings estimate remaining unchanged for Oil India.

But, even with higher crude prices during FY18, the research house has lowered its earnings per share estimate by nine per cent each for Cairn India, Oil India and ONGC. They arrive at a target price of Rs 134 for Cairn, Rs 446 for Oil India and Rs 233 for ONGC. The consensus target price as per analysts polled in March for ONGC, Oil India and Cairn stands at Rs 230, Rs 388 and Rs 153, respectively.

It has introduced a uniform licence for all fuels (natural gas, crude oil or shale gas). Explorers (upstream entities in sector jargon) get the freedom to price petroleum products procured from hard-to-explore deep waters at market rates. Some licences for small and medium size fields have been extended and production sharing contracts for many have been extended till the economic life of such assets.

This is positive for the sector, as it removes anomalies and will accrue benefits in exploration activities but in the long run.

In the near term, it will not have much impact on companies’ earnings, say analysts.

Thus, the scrip of government-owned upstream entities such as Oil and Natural Gas Corporation (ONGC) and Oil India did not react much, closing at Rs 205.70 (up 0.3 per cent) and Rs 309.55 (up 0.06 per cent), respectively, on Thursday.

The bigger news has been the sharp rise in oil prices, from $33 levels at end-February to $40 a barrel. The stocks have gained significantly, with ONGC up six per cent and Cairn India by 21 per cent from their lows on Budget Day. Oil India has not seen much rise, due to concerns on production from maturing fields. Nevertheless, higher crude oil prices are always beneficial for producers.

Analysts do not see oil prices rising significantly in the near to medium term. They see it averaging $45-50 in FY17, similar to the levels in FY16. It is only from FY18 that analysts expect a recovery in crude oil prices. For instance, analysts at HSBC estimate $45/60/75 a barrel in FY17/18/19, respectively. With revised cess rates, they see a three per cent rise in FY17 earnings for Cairn India, a one per cent negative impact on earnings for ONGC and the earnings estimate remaining unchanged for Oil India.

But, even with higher crude prices during FY18, the research house has lowered its earnings per share estimate by nine per cent each for Cairn India, Oil India and ONGC. They arrive at a target price of Rs 134 for Cairn, Rs 446 for Oil India and Rs 233 for ONGC. The consensus target price as per analysts polled in March for ONGC, Oil India and Cairn stands at Rs 230, Rs 388 and Rs 153, respectively.