"Margin topping adds to Jubilant FoodWorks show")

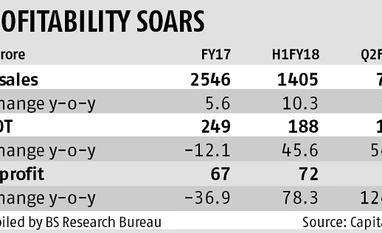

Jubilant FoodWorks reported a better-than-expected September quarter performance. The operating profit margin at 14.1 per cent was up 450 basis points year-on-year, the highest in 14 quarters. It was led by revenue performance and cost optimisation. Most analysts had estimated the margin number at 12-12.5 per cent.

Operating profit jumped 59 per cent over a year to Rs 102 crore; revenue grew nine per cent to Rs 726 crore. This was led by strong growth in volumes and a 5.5 per cent same-store sales growth (SSSG). The top line growth would have been better considering that the company passed on GST benefits (two per cent reduction in tax) by reducing prices.

Passing on of input credit gains to customers in the form of more product additions (toppings) at the same value and absorbing the food inflation also helped. Profit after tax was up 124 per cent to Rs 48.5 crore with net margins at 6.7 per cent.

SSSG was led by continued traction from the everyday value offering launched in the first quarter and the new Domino’s campaign in August. It was, however, lower than analysts’ estimates of 7-7.5 per cent growth. SSSG was 6.5 per cent in the June 2017 quarter and 4.2 per cent in the June 2016 one.

Analysts had estimated five or six new stores in the quarter but the company has become conservative on this. It added one Domino’s store and shut another, ending the September quarter at 1,125 (1,081 a year before), the same as at the start. Store additions are to follow a more exhaustive criteria.

Analysts had estimated five or six new stores in the quarter but the company has become conservative on this. It added one Domino’s store and shut another, ending the September quarter at 1,125 (1,081 a year before), the same as at the start. Store additions are to follow a more exhaustive criteria.

There is a focus on cost management by higher personnel utilisation and improved productivity, while cutting on administration and promotion expenses. Lower other expenses in the quarter were, for example, a function of what the company called optimising of advertising cost.

The other area the company is focused on is cutting the loss on its Dunkin’ Donuts franchise. The company continues to rationalise the store portfolio of this brand, having closed five and added two, taking the total at the quarter's end to 52. That number stood at 73 in the year-ago quarter. It expects to reduce losses by half in FY18 from this business and see break-even in FY19.

Himanshu Nayyar, analyst at Systematix Shares, said, “If you look at same stores sales are almost same on q-o-q basis, we could see good margins at Ebitda (earnings before interest, tax, depreciation and amortisation) level and it shows that the cost control measures are showing some results.”

However, there are no stores opened during the quarter, this may be the reason for no substantial increase in their cost structure. If this kind of profitability is delivered, there is definitely upside for this stock, he said.

The strategy, clearly, is on opening new stores selectively and to drive SSSG from existing ones. Coupled with everyday value offerings, this is expected to drive volumes, growth and profit. While there is scope for margins to improve, the company is investing in technology to improve customer experience (online and offline) and reduce cost, while scaling up operations. This and rising input cost could keep a lid on the margins.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in