"Maruti: One-offs take shine off top line; volume outlook remains strong")

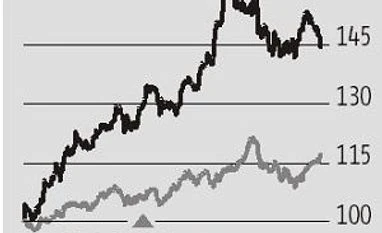

Maruti Suzuki’s March quarter numbers were a mixed bag. While the top line, led by strong volumes and higher realisations, came in better than estimates, the operating performance pegged back by higher operating expenses dented margins. One-off interest costs led to lower net profits, which came in below estimates. The stock, which has gained about 38 per cent over the past year, shed 2 per cent after the results were announced.

There is, however, nothing to complain about as far as volume performance is concerned. Even as the sector struggles with single-digit growth, consumers can’t have enough of India’s largest carmaker. Led by a 11.4 per cent increase in volumes which include models with a waiting period and three per cent higher realisations, the company’s revenues, at Rs 205.94 billion, was in line with analysts’ estimates.

Volumes and average selling prices are on the higher side given increasing demand for premium cars and utility vehicles. While overall volumes continue to be driven by the compact segment (Ignis, Baleno and Dzire, among others) which accounts for 45 per cent of volumes, sales growth of utility vehicles is the highest both for the quarter and the year. Ertiga, Vitara Brezza and S-Cross have helped the company gain over 27 per cent share in the segment for FY18, with volume growth for the first two models at 36-44 per cent for the full year.

The company seems confident of maintaining double-digit growth with both rural and urban markets contributing to FY19 volumes. The rural sector, which accounts for 36 per cent of the sales, is growing at a higher clip (16 per cent) than the urban segment and expectation of a normal monsoon, improving farm incomes and rural infrastructure is expected to rub off positively on sales, given Maruti’s brand and distribution leadership.

The other area the Street will look at is falling royalty rates which came in at 5.4 per cent of sales for FY18 as compared to 5.8 per cent in the previous year. The management indicated that for models launched after January 2017 (Ignis, Dzire and Swift) royalty paid will be in rupees which will trend down as volumes improve.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in