"More pain ahead for drug makers in FY19 after a challenging FY18")

If FY18 was a forgettable year for the pharma sector, FY19 might not be any better. This is on account of improved pace of approvals from April 1, 2018 as well as competition even for drugs, which are difficult to make. New guidelines from the US Food and Drug Administration had led to the slowing down in drug approvals over the last couple of months as companies took time to adjust. However, as companies comply with the new guidelines, the approval time for drugs from April is expected to come down further increasing competitive pressures. Anubhav Aggarwal and Chunky Shah of Credit Suisse believe that as first cycle approvals (after the first inspection) increase further, the period of high profits on few drugs should shorten and impact industry profitability significantly. They expect a 50 per cent increase in ANDA approvals over the next two years and price erosion to be high in double digits.

What is adding to the disappointment has been the lack of steady and consistent compliance record on the manufacturing front. The record has worsened given the observations by the US FDA in recent inspections. Glenmark, Lupin, Aurobindo, and Cipla who have had a strong track record in US FDA objections have seen manufacturing violations at their key facilities in recent months. Harith Ahamed and Krishna Prakash R of Spark Capital say that the repeat nature of observations and inability to resolve issues completely at critical sites, even post 12-15 months of remediation and engagement with third-party consultants have disappointed investors. Shifts in the nature of inspectional observations flagged by FDA at Indian sites have added to the concerns, they added.

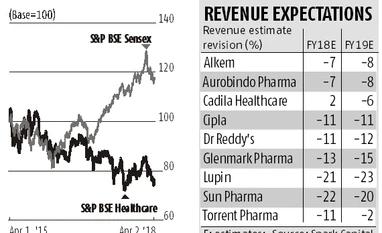

Companies in the sector were banking on complex or difficult to make generics as well as sales under exclusivity to overcome the stiff pricing pressures on their base business. The progress on this front at best has been gradual. Competitive intensity has increased substantially in segments where Indian players have made large investments such as dermatology, ophthalmology, oncology and hormonal drugs. Analysts at Spark Capital say meaningful monetisation of opportunities will require significantly better execution than in the recent past.

Sun Pharma (and its partner Merck), for example, recently got an approval for tildra, a new biological entity for treating inflammatory disorders after completing the necessary clinical trials. While the opportunity size is large, the company, according to Kotak Institutional Equities faces steep commercial hurdles and higher promotional activity given a number of competing drugs. After years of collaboration, the pay off thus becomes unpredictable and depends on the ability of the product to gain traction backed by strong execution. For Cadila Healthcare, sooner than expected competition from Teva and Mylan for Lialda (ulcerative colitis) means that a product which was expected to have limited competition will translate to lower profits going ahead. Among other drugs, the company is also facing pressure in potassium citrate (kidney ailment) given competition from Strides Shashun and Teva. While there are some niche opportunities for the company such as Toprol and launch pipeline for FY19 is strong (40 ANDA launches), Cadila has the highest price erosion risk as 45 per cent of its US revenues comes from its top three products.

Given the regulatory challenges, higher product approvals from April and payoff from complex/niche generics not able to compensate for the high base business erosion, investors should await more clarity especially consistent revenue growth from US market. Don’t take an exposure only on the basis of lower valuations.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in