"EV shift, margins near-term headwinds for Bosch")

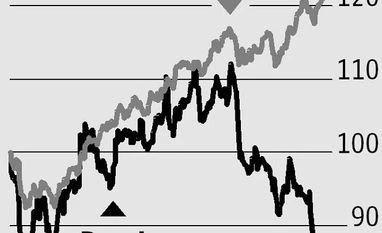

The Bosch stock has shed 10 per cent over the last fortnight on muted September quarter results, and lower-than-expected revenues from the transition to BS-IV emission norms. Analysts say that BS-IV average selling prices were lower than originally estimated in the September quarter, which led to the steep underperformance on the top line front. Revenues grew just under 7 per cent year-on-year (y-o-y) to Rs 2,811 crore, while analysts had estimated it to grow over 31 per cent to Rs 3,421 crore.

What made matters worse was lower revenue in the replacement market segment (20 per cent of revenues), which were muted due to the implementation of the goods and services tax (GST). Consequently, analysts have cut their estimates for Bosch.

Compiled by BS Research Bureau

The other concern stems from the expected shift towards electric vehicles (EVs), and challenges for the Indian arm of the Germany-based Bosch AG. Currently, diesel engines account for 60 per cent of the company’s revenues and the pace of transition to EVs would be crucial for the company. However, analysts say worries on this count have been addressed as of now, as Bosch AG recently indicated it planned to commercialise electric mobility-related technologies through its listed arm.

Analysts at UBS say this significantly enhances the long-term outlook for Bosch, and elevates any concerns of the negative impact from the shift towards EVs, and away from diesel systems in the long term. This, according to the brokerage, could sustain higher price-to-earnings multiple for the company, given that it would be a unique firm, in the Indian context, with access to high-end global electric mobility technology.

In the near term, there are two triggers for the company: First is growth in the medium and heavy commercial vehicle (M&HCV) space, with margins being the second. Volume growth for the sector had moderated in October (1 per cent y-o-y growth), against 26 per cent y-o-y growth in the September quarter. Analysts say growth should be better going ahead, given that October 2016 had a higher base. Margins in Q2FY18 were down 58 basis points due to higher costs of the imported content for BS-IV, and increase in commodity costs. Analysts expect margin pressure to remain till localisation levels improve.

Given the current valuations, and near-term headwinds, investors should wait for an improvement in M&HCV volumes, as well as overall margins before considering the stock. The next major regulatory trigger for the company would be the transition to BS-VI standards for emission norms from April 1, 2020.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in