"Jio-led price wars halve Bharti Airtel Q3 profit to Rs 504 crore")

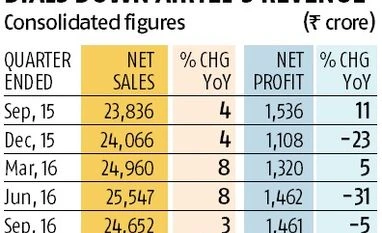

Bogged by competitive pressures brought on by low tariffs of Reliance Jio (RJio) and disruption due to demonetisation, Bharti Airtel’s December quarter (Q3) numbers were below Street estimates. Pricing pressure in India coupled with Nigerian currency devaluation saw consolidated revenues fall three per cent year-on-year (y-o-y) to Rs 23,336 crore, compared to Bloomberg consensus estimates of Rs 23,897 crore.

Adjusted for divested Africa units, the sale of tower assets and Bangladesh merger, revenue performance was flat. According to Bloomberg, this was the worst-ever revenue growth performance for the company. Operating profit at Rs 8,570 crore was up just 1.1 per cent though lower than estimates of Rs 8,760 crore due to subdued performance.

Net profit, too, fell by more than half to Rs 504 crore and came in lower than consensus estimates of Rs 1,023 crore, on account of a 33 per cent increase in net interest costs (higher debt due to spectrum purchase) as well as higher spectrum amortisation and depreciation cost, which were up 11 per cent over the year-ago period. The company’s consolidated debt after the October 2016 spectrum auction, when it acquired rights to airwaves worth Rs 14,281 crore, has increased to $14.3 billion (Rs 97,500 crore), from $12.2 billion in the September quarter.

Acknowledging the pricing pressures, Gopal Vittal, managing director and chief executive officer, India & South Asia, Bharti Airtel, said the quarter has seen turbulence due to the continued predatory pricing by a new operator. “The present termination costs at 14 paise, which are well below cost, have resulted in a tsunami of minutes terminating into our network. This has led to an unprecedented y-o-y revenue decline for the industry, pressure on margins and a serious impact on the financial health of the sector.”

But, the deepest cuts are in the faster-growing data segment. Not only was the realisation down over 11 per cent sequentially, volumes, too, fell 3.5 per cent over the September quarter. Analysts at IDFC Securities had highlighted the negative impact of demonetisation on prepaid recharges, specifically data volume growth. Data, as a percentage of mobile service revenues, which have been on an uptrend since 3G services took off, fell 200 basis points sequentially to 22.8 per cent.

The positive aspects from the results are the Africa operations, where revenues grew six per cent YoY, the highest in the past nine quarters. Data revenues at $153 million were up 24 per cent over the year-ago quarter, led by increase in data customer base of 21.3 per cent, while data volumes were higher by 91 per cent. Africa contributes 23 per cent to consolidated revenues.

Going ahead, in addition to the RJio impact, the Street will keep an eye out for deals such as the acquisition of five circles of Telenor by Bharti Airtel. Telenor operates in seven circles, including Maharashtra and Gujarat, and the circles contribute around 37 per cent to Bharti’s revenues.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in