"Shoppers Stop: Lower volumes and muted same-store sales dent Q4 performance")

Shoppers Stop reported a muted March quarter (Q4) performance due to lower volumes and same-store sales (SSS) growth. This dragged down the top line by 7 per cent as compared to the year-ago quarter. SSS was down 4.1 per cent given the change in goods and services tax (GST) rates and thus lower price of some items, change in promotional period and mall renovations.

The management had earlier indicated that its top line could see some pressures on account of ongoing renovations and road construction, which would impact its footfalls for key stores. It is not surprising then that footfalls declined 9 per cent. What aggravated the situation was the continuing correction in private label inventory as well as product mix. The company could not meet its FY18 SSS growth guidance of 4 per cent due to higher competition, reduced retail prices, renovations and private label changes and had to be content with SSS growth of 2.1 per cent.

Falling revenues and higher costs limited any scope for margin expansion. Margins came in at 6.1 per cent, below analysts’ estimates which had pegged it at 6.4 per cent. But, on a full-year basis (FY18), cost control initiatives helped the company improve margins to 5.9 per cent, which is 60 basis points higher than FY17.

shoppers stop

What was positive, however, has been the improvement in net profit on the back of lower interest and taxes. The company’s efforts to bring down debt has helped with debt coming down from Rs 3.65 billion to Rs 470 million, as of March 31. Given the 77.5 per cent decline in interest costs as well as lower taxes, adjusted net profit came in at Rs 208 million, up 77.2 per cent over the year-ago quarter. Analysts expect lower debt to improve the earnings of the company in FY19 and FY20.

On the operational front, the management expects SSS growth to improve with guidance for FY19 at 7.5 per cent. Analysts at Emkay Research believe the re-jigging of private labels, improved in-store experience and digital programmes should help drive footfalls and SSS in FY19. SSS growth over the next two years is pegged in the 5-8 per cent range.

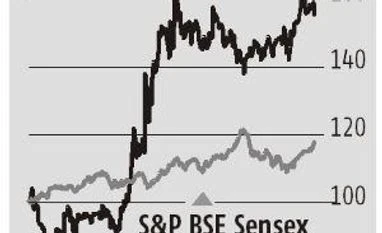

At the current price, the stock is trading at 50 times its FY19 estimates. Though it is expected to be an improvement in operating metrics this year, investors should await the sustained trend of SSS growth in the coming quarters and better valuations before taking an exposure to the stock.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in