"Slowdown in TCS to weigh on Tatas' growth ambitions")

Tata Consultancy Services’ (TCS’) revenue growth in 2016-17 was the slowest since 2008-09. For the first time since its stock exchange listing in 2005, both revenue and profit growth was in single digit for the software major.

This, say analysts, could impact Tata group’s growth plans. TCS’ cash generation has helped the Tatas maintain a growth streak despite poor profitability at the rest of the group since the 2008 global financial crisis.

On the previous occasion, the company experienced a V-shaped recovery. This time, analysts see a structural slowing in the information technology (IT) sector worldwide, leading to sub-par growth for TCS. “I don’t foresee any immediate pick-up in IT sector growth for at least two years. This would translate into single digit growth for most Indian IT companies during the period,” says G Chokkalingam, chief executive at Equinomics Research & Advisory.

Earlier this month, Gartner, the US-based research and advisory entity for the sector, cut its estimate of worldwide IT spending growth in 2017 to 1.4 per cent, from its earlier forecast of 2.7 per cent.

This would translate into lower growth for TCS. And, hurt the dividend income for its parent, Tata Sons, the group holding company.

Tata Sons owns 73 per cent of the equity in TCS, the highest among listed group companies. Dividend income from the latter has been the prime source of revenue and profit for the holding company in the past decade. This cash finds its way to various group companies, listed and unlisted, as incremental equity investment.

Tata Sons is estimated to have cumulatively earned nearly Rs 45,000 crore worth of equity dividend from TCS since its listing in 2005. Beside, the holding company has raised capital in the past by either divesting its stake in the company or pledging a part of its TCS holding with lenders. Tata Sons owned 80.64 per cent stake in TCS in the last quarter of 2004. In the period, Tata Sons made incremental equity investment of Rs 46,500 crore in group companies, of which around Rs 25,000 crore went to listed ones. The figure includes preference shares and debentures.

Equity support from the holding company allowed group companies to invest in growth, despite an adverse operating environment.

“Explicit or implicit equity support from Tata Sons is a key source of financial strength for group companies. This is especially true for Tata Steel, Tata Power and Tata Teleservices, facing financial and economic headwinds for many years,” says Chokkalingam.

The group’s other listed companies cumulatively made around Rs 3 lakh crore of capital expenditure in the past decade — nearly three times their cumulative retained earnings in the period. This translates into an annual capex of Rs 27,000 crore on average since 2004-05, against annual average retained earnings of Rs 8,700 crore in the period. They funded the rest from incremental borrowing, the equity support coming from Tata Sons.

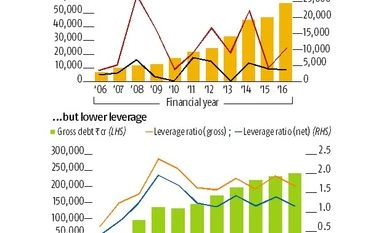

The group combined (excluding TCS) debt to equity ratio (on a gross basis) declined to 1.67 in FY16 from 1.94 in FY15 and a record high of 2.4 in FY09. The net debt to equity ratio was down to 1.16 in FY16 from 1.38 in FY15 and a record high of 2 in FY09. In comparison, the group’s gross debt doubled during the period from Rs 1.1 lakh crore in FY09 to Rs 2.4 lakh crore at the end of FY16; group assets jumped from Rs 2 lakh crore in FY09 to Rs 4.35 lakh crore in FY16.

Analysts say the group’s dependence on TCS would reduce if other large companies such as Tata Motors or Tata Steel show strong improvement in earnings. Tata Steel is expected to report better numbers in the future but it has to be seen how much of dividend it can spare, given its own capex requirements. Tata Motors is the second most profitable entity in the group, after TCS. However, it is currently implementing an ambitious capex plan in both its domestic business and the Jaguar Land Rover division abroad.

In sum, there is no getting away from TCS in the short to medium term for the group.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in