TCS bets on digital, banking to revive growth as Q3 net rises 11%

Revenue up 8.7% in volatile business environment

"TCS bets on digital, banking to revive growth as Q3 net rises 11%")

premium

WebinarsNew

Deep DiveNew

Explore Business Standard

Revenue up 8.7% in volatile business environment

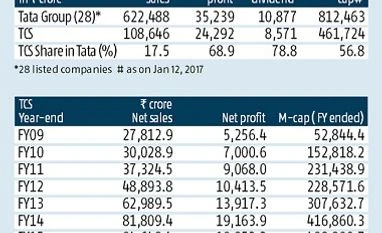

Tata Consultancy Services (TCS), the country's largest software exporter, said third-quarter (Q3, September-December) profits grew 11.2 per cent from a year before to Rs 6,778 crore, with higher growth from digital services, mainly via banking customers which have resumed spending on technology to compete in a digital environment.

Revenue grew 8.7 per cent to Rs 29,735 crore, on strong execution and a 30 per cent jump from digital services. TCS had reported profit of Rs 6,125 crore on revenue of Rs 27,364 crore in the quarter to December 2015. Operating margins were 26 per cent, which the company said it would maintain, at 26-28 per cent.

However, in dollar terms, revenue grew only 2.2 per cent to $4.39 billion, with total growth in the year at 5.3 per cent. Last year, TCS reported 7.1 per cent revenue growth, the lowest in six years.

"The resilience of our business model and strength of our operating strategy has been brought to the fore by our performance in Q3, traditionally a quarter with weak demand,"said N Chandrasekaran, managing director.

TCS is the first major Indian information technology (IT) services company to declare its quarterly results, keenly watched by both local rivals such as Infosys and Wipro, and global ones such as IBM and Accenture, as they see lower growth in traditional business due to technology shifts such as digital and cloud. Smaller rival Infosys, headed by its first non-founder chief executive officer, Vishal Sikka, will announce its results on Friday.

"Constant currency (growth) is disappointing. We were expecting 2.9 per cent and it came at two per cent. The TCS stock movement now depends on Infosys. If Infosys reports a just in-line set of numbers tomorrow, I expect the TCS stock will trend downwards. An accumulate rating on TCS now, with a target price (estimate of where the scrip will go) of Rs 2,620," said Ravi Menon, IT analyst at Elara Capital.

Others say TCS had met expectations in a volatile business environment, which has seen shifts in technology adoption and the change in political climate in America. 'We did not expect it to be a beat (on expectations). They delivered on muted expectations. The BFSI (banking, financial services and insurance division) commentary is pretty positive. The management is confident of maintaining the margin range, despite and in spite of visa wage bills increasing, surprising and a key positive," said Ashish Chopra, IT analyst at Motilal Oswal Securities. "How they do it is something we need to watch but that comment in itself will be construed positively, as that has been a key overhang on the valuations of IT companies."

TCS expects any improvement in the US economy would help the company to grow, despite President-elect Donald Trump's plans to curb outsourcing, as it is the largest local IT services employer there.

"On US (legislature) Bills, there are two themes on what has come and what can come. One is the restriction on the number of visas and the second is the increase in minimum wage. If you account for the very low number of visas we took, we should have already suffered; we had to compensate for the lack of those visasure and that gives us confidence," said Chandrasekharan.

The stock closed on Thursday at Rs 20.25 or 0.9 per cent higher at Rs 2,343.30 on the BSE.

Already subscribed? Log in

Subscribe to read the full story →

3 Months

₹300/Month

1 Year

₹225/Month

2 Years

₹162/Month

Renews automatically, cancel anytime

Over 30 premium stories daily, handpicked by our editors

News, Games, Cooking, Audio, Wirecutter & The Athletic

Digital replica of our daily newspaper — with options to read, save, and share

Insights on markets, finance, politics, tech, and more delivered to your inbox

In-depth market analysis & insights with access to The Smart Investor

Repository of articles and publications dating back to 1997

Uninterrupted reading experience with no advertisements

Access Business Standard across devices — mobile, tablet, or PC, via web or app

First Published: Jan 13 2017 | 12:47 AM IST