"TCS plans India's biggest buyback, puts spotlight on Infosys cash pile")

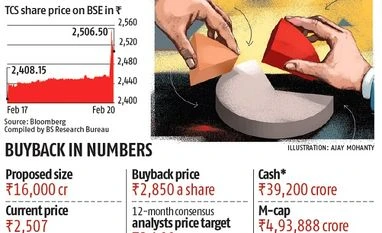

Tata Consultancy Services (TCS), the country’s highest-valued company on the stock market, announced a buyback of shares worth Rs 16,000 crore, the biggest ever in the Indian capital market.

Under the programme, approved by its board of directors, the software services major will repurchase 56.1 million shares (2.85 per cent of its equity) at Rs 2,850 apiece.

The buyback price is 13.7 per cent higher than TCS’ current market price and an 18.3 per cent premium to Friday’s close. Shares of the company soared after the announcement to end at Rs 2,506.50, about four per cent higher than its previous close.

Market players said further gains in the stock price could be capped because the premium offered was in line with that given by information technology (IT) firms such as Wipro and Mphasis.

Analysts say as the buyback is only 2.8 per cent of its equity, the earnings per share (EPS) might not get a boost. Shares purchased through buybacks are extinguished, which typically improves financial metrics like EPS. But, since Rs 16,000 crore worth of cash equivalent will be utilised for buyback, the interest income (assuming yield of about six per cent earned on this money), which reflects in the company’s other income, will also cease to exist. This is equivalent to three per cent of TCS’ pre-tax profit. However, its return on equity (RoE) is set to see a jump, as cash typically delivers lower returns.

Ashish Chopra, IT analyst at Motilal Oswal Securities, estimated the buyback to improve TCS’ RoE by 250 basis points, to 36 per cent, in FY17. TCS had paid a dividend of Rs 8,700 crore in FY16 and its highest-ever of Rs 15,500 crore in FY15. Most analysts, viewing the move as in the right direction, said TCS should consider buybacks more frequently.

Credit Suisse’s IT analyst Anantha Narayan said a one-off buyback might not help TCS much. “A consistent payout policy can be used to value the stock better on cash flows. Such a policy has not been announced at this time but could be with the fourth quarter results”.

Factoring in the buyback, the current financial year is likely to go down as the most rewarding for TCS shareholders. The IT major, with a cash pile of Rs 39,200 crore, has paid dividend of Rs 3,842 crore so far in FY17 (Rs 6.5 per share at the end of every quarter).

“The upshift in payout is a definite positive for the valuation multiple of TCS, considering the high yield from dividend and buyback combined. At the moment, Rs 81 per share of buyback comes over and above our expectation of Rs 45 dividend this year,” said Chopra.

Analysts see the buyback as a move by TCS to realign its capital allocation strategy with global peers such as Accenture and Cognizant. Accenture returned over 100 per cent of its free cash flows to shareholders via buybacks and dividends. Cognizant recently stepped up its payout policy and plans to pay about $3.4 billion over the next two years, nearly 100 per cent of the free cash flows it generated in 2016.

Analysts say the TCS buyback will now put Infosys in the limelight, having a similar cash pile as its bigger rival.

The buyback will be through the so-called ‘tender route’, which allows promoters to tender their shares. The mega buyback could result in a Rs 11,700-crore benefit for Tata Sons, which owns 73.33 per cent in the company, assuming all shareholders submit their entire holdings for buyback.

Interestingly, monetising a three per cent stake in TCS to raise Rs 14,700 crore was part of Tata Sons business plan for the next five years. It remains to be seen if this would partly alleviate that need.

Higher payouts via buybacks also make sense given the slowing growth as well as acquisition-shy nature of Indian IT companies. Buybacks are also more tax-efficient than dividend payouts.

Apurva Prasad, IT analyst at HDFC Securities, said, “Accenture did acquisitions worth $1.7 billion in the past two years versus entire Indian IT acquisition put together at $2.3 billion. Comparing these facts, the imperative to pay out more is there for Indian IT.

Revenue growth of Indian IT companies is likely to moderate to high-single digit. For FY16-19, we expect TCS to post 8.2 per cent CAGR in its dollar revenue, versus 8.7 per cent by Infosys and 6.3 per cent by Wipro. HCL and Tech Mahindra could post 11.3 per cent and 9.9 per cent, respectively.”

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in