"Beyond Barmer: Vedanta continues to struggle on other projects")

So much so that in July it came to light that Cairn Energy had extended a loan of $1.25 billion to a subsidiary of Sesa Sterlite. Out of this, $800 million had already been disbursed. While investors weren't enthused and analysts raised the red flag, the company said it was a wise investment because the loan was extended at 300 percentage points over the London inter-bank offered rate, which was more than what a fixed deposit in a bank would have fetched, and it wouldn't result in a resource crunch because the company's three-year investment outlay of $3 billion was adequately funded.

One news report quoted the Cairn India spokesperson arguing that the loan wasn't a material transaction because it did not exceed 5 per cent of the company's annual turnover or 20 per cent of its net worth, and hence did not require the shareholders' approval. Tom Albanese, chief executive officer, Vedanta Resources, dismissed investor concerns in an interview with Business Standard. "Board members of Cairn India who were associated with Vedanta or Sesa Sterlite weren't part of this decision. It was decided this (extending the loan) was a better return on the funds Cairn had, over and above what was needed for operations. The decision was taken at the board level and was consistent with the rules and regulations of corporate governance," he said.

Life Insurance Corporation, the second largest shareholder in Cairn India, too had questioned the inter-company loan given for two years. Analysts say the company pushed for the loan before the rules relating to related-party transactions were notified. Under the new Companies Act, shareholder approval for such transactions is required. Cairn India, however, had earlier said this being a related-party transaction, approval of the audit committee was taken and the transaction had been effected on arm's-length principal. While the debate continues, the importance of Cairn India for Vedanta Resources cannot be overemphasised, especially keeping in mind that at the beginning of the current financial year, Vedanta Resources's consolidated debt stood at almost $17 billion.

In a bind

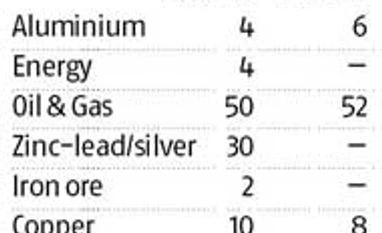

The group's other companies face serious regulatory challenges, especially its operations in India. The Iron ore business, for instance, was crippled due to the ban imposed by the Supreme Court on mining following the Shah Commission report on irregularities in the allotment of mines. The segment is now regaining momentum after the ban in Karnataka was partially lifted last year. The ban in Goa was lifted only last month. Though the group says it is still working with the Goa government and the Centre's ministry of environment and forests to restart mining, Fitch expects the process for securing other regulatory approvals related to mining in Goa to continue to impact the company in the near term.

That leaves the task of boosting the cash flow to Cairn India alone. "The group had a high level of debt and assets, too. It, therefore, leveraged its buy-outs. Right now, Cairn India is the only big cash flow generator. And, its acquisition has gone down pretty well with the group," says Girish Shirodkar, managing partner (India and Asia Pacific), Strategic Decisions Group, a global consultancy dealing in strategic decision-making, risk management and shareholder value creation. He said since there was a debt overhang, the focus is more on dealing with it than on investing in the future. "This raises the issue of corporate governance and poor level of transparency."

Besides, analysts worry that Cairn India is focussing only on its flagship asset at Barmer in Rajasthan, as against investing in other properties. And the future of the Barmer block is itself undecided. The Barmer asset contributed 83 per cent to the company's total production of 218,651 barrels of oil equivalent a day, but what is worrying for the company is that the government is yet to take a call on granting extension to its production sharing contract for the block. Cairn India had submitted an application to the Union ministry of petroleum and natural gas for an extension on April 5, 2013.

Under Article 2.1 of the production-sharing contract, Cairn's rights over the block are for a period of 25 years which end in 2020. It can get an extension for five years in the normal course of business; in the case of natural gas production, the extension can be for 10 years. The company had announced $3 billion net capital expenditure programme to fuel growth till 2017 for the block. In order to make further investments, the company has to submit a field development plan, laying out all the project details, estimates of development costs and production costs, and the production profile, among other things. Since it will determine the economics of the project, the plan can be developed only till the duration of mining lease or the production-sharing contract period, even though the field is capable of producing for additional 10 or even 20 years. A committee in the ministry of petroleum and natural gas will take a call on the extension.

When asked about the group's dealing with Cairn India and the plans for it, a Vedanta Resources spokesperson did not answer queries, citing company policy of not making forward-looking statements. Shirodkar of Strategic Decisions Group, however, says though it is good for the group to have access to some cash flow until such time as it is able to get debt and equity right, any financial dealing within the group should meet the corporate governance norms. For Vedanta Resources, if the uncertainty surrounding Barmer clears up, and iron ore mining picks up, not only will its cash flow situation improve, but it would also reduce its excessive dependence on Cairn India - Barmer in particular.