"Why are we shorting Amazon stock again?")

Preamble

In last quarter of 2016, (October 2016), our algorithms gave a strong signal to short sell the Amazon (NASDAQ:AMZN) stock. We correctly called the top at $844 on 5 October, 2016. (Read more)

On 28 October, 2016, the Amazon stock corrected sharply by over 5% to close at $776. We were very categorical that the stock has risen and has peaked and would correct sharply. We were proven correct on our call to short Amazon stock. EquNev-K1t Capital Hedge Fund is a quant long-short hedge fund that operates on S&P 500 stocks. (Read more)

Our strategy has always been mean-riveting and our calls on the markets have always proved correct. So what has changed now on Amazon that we are short selling again?

Amazon over the last 2 quarter of 2017

In the last 2 Quarters of 2017, Amazon has delivered a lower operating margin, aggressive expansion in India (they are still burning cash, more on the India e-commerce sector later), the rapid proliferation of its Alexa voice assistant, and more advanced and efficient robotics, the overarching theme at Amazon remains largely the same: The company wants to capitalise on all of its best long-term opportunities, even if it means lower profit margins currently. Amazon continued to impress investors when it reported its 27 April 2017 first-quarter earnings. The report highlighted rapid growth, improving cashflow, and aggressive spending on growth opportunities, sending shares to new highs. But the key question remains: Is the price sustainable given its recent performance over the last two quarters?

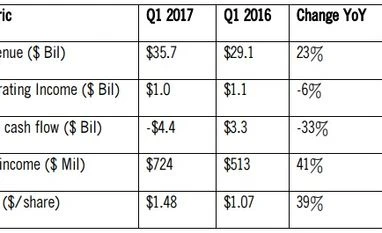

Quarterly performance numbers

Amazon reported results for the first quarter of fiscal year 2017 in April 2017. The report was welcomed with a 4% share price boost in after-hours trading, as the company breezed by management's guidance targets for the quarter. The key financial numbers reported are as under:

Key factors and metrics for analysts' price revisions

While there are several stock market analysts who have given a call for upward revision of Amazon stock price to close at $1,100 by year-end 2017. Some of the factors whether Amazon will meet or miss its 2017 year-end target that need to be considered here are as under

Rapid sales growth

Amazon's net sales in its first quarter continued to rise quickly. First-quarter revenue hit $35.7 billion, up 23% year over year. This increase was driven primarily by Amazon's 24% increase in its North America e-commerce sales, but also benefited from revenue growth internationally and in its cloud services.

Amazon Web Services (AWS) growth

AWS, saw sales rise 43% year over year, followed by 24% revenue growth in the North American online platform. AWS accounted for 10.2% of Amazon's total sales in the quarter, up from 8.8% in the year-ago period. The AWS segment also increased its operating income by 47%, landing at $890 million.

Operating cash flows

Given major fluctuations in Amazon's aggressive spending on growth opportunities, management understandably likes to track its operating cash flow on a trailing-12-month basis. In its first quarter, Amazon said operating cash flow was up 53% in the trailing 12 months compared to the year-ago period. Operating cash flow hit $17.6 billion, up from $11.6 billion in the year-ago trailing-12-month period.

Operating losses internationally

Not all key metrics are headed upward at Amazon. In the company's first quarter, its international operating loss widened from $121 million in the year-ago quarter to a loss of $481 million, despite international net sales during this period increasing from $9.6 billion in the first quarter of 2016 to $11.1 billion in the first quarter of 2017. Amazon's wider loss internationally comes as the company aggressively expands its offerings overseas, namely in India where Amazon has increased its Prime selection by 75% in the last 3 quarters

Investments in India

Amazon is still pushing hard into the large market for e-commerce in India and investing despite the shake up in the Indian e-commerce sector. "Our India team is moving fast and delivering for customers and sellers," said Amazon CEO Jeff Bezos in a prepared statement. "The team has increased Prime selection by 75% since launching the program nine months ago, increased fulfillment capacity for sellers by 26% already this year, announced 18 Indian Original TV series, and just last week introduced a Fire TV Stick optimised for Indian customers with integrated voice search in English and Hindi."

Rapid growth in Amazon Prime customer base

Piper Jaffray which revised the price target upwards says that Amazon Prime is now subscribed to by somewhere in the mid-to-high 60 million households range - and the service has signed up about 10 million new households over the past year alone (about 20% year-over-year growth).

Growth in online and offline retail business

Needham & Co which revised its price target more aggressively believes that Amazon owns a 34% share of the U.S. retail market - nearly seven times larger than Wal-Mart does. But here's the really astounding part: According to Needham, over the next five years Amazon.com is likely to add 16 more percentage points of market share to its domain, giving Amazon a clean sweep of majority market share.

These are some of the factors for which analyst and investors are bullish about Amazon. Like last year, would the price targets be met on Amazon? We don’t think so.

Indian e-commerce sector sees red

As capital raising tap dries up for the Indian e-commerce sector, there are signs of consolidations and shut downs. While there is consolidation on the anvil, newer players like the Mukesh Ambani’s Reliance Group with the advanced internet infrastructure built by Jio, and a robust physical retail built by Reliance Retail, planning to create a differentiated e-commerce model for India. The path to profitability for Amazon in India may just grow a bit longer and be unsettling.

The positive face put up by the Snapdeal promoter last year when we were travelling together back from San Francisco as a 6-month cycle has finally snapped and there is no positive investor interest in them or the e-commerce sector as a whole in India.

Amazon Prime – a new war front in India

While Amazon launched its Prime in July 2016, it is still burning cash on advertising and content acquisition. The impact of these expenditures and investments are already showing on lower profitability on Amazon’s consolidated profitability being dragged by the losses on the international business due to Prime.

Would Amazon be the tech giant that will see a correction?

Apple, Amazon, Facebook, Microsoft and Alphabet, the parent company of Google, are not just the largest technology companies in the world. These companies are also becoming the most powerful companies of any kind, essentially inescapable for any consumer or business that wants to participate in the modern world. Earlier last year, Warren Buffet bought into Apple. In their recent disclosures, they also hold investments in Amazon, Alphabet (Google) also. But which of the Frightful Five is most unavoidable? Check out the comparisons

Why are we short selling Amazon again?

As positive uptrend on Amazon continues with some of the major brokerages which have rerated the year-end price target for Amazon, we have an opportunity to short Amazon once again. We are also expecting sharp corrections in the wider market. Should both the events trigger off, we could see the price of Amazon stock to drop below even $800 in the next few months. Hence the ride from there till the year-end price targets put out by some of the analysts may again see a miss!

Lets wait and watch! We have so far not been proven wrong on Amazon!

The author is Director, EquNev-K1T Capital Hedge Fund, a US equity market-focused Indian hedge fund and Managing Partner, India Healthcare Opportunities Fund

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in