"Wipro, HCL Tech outshine TCS and Infy in March quarter")

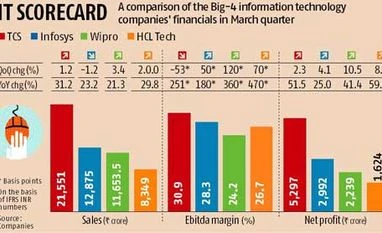

Healthy deal pipelines, cost efficiencies and improving utilisation rates drove the revenue and earnings growth of the three IT majors. While Infosys continued to be cautious on client spending and discretionary budgets, the managements of the other three were positive on 2014-15 growth. While TCS and HCL Technologies expect this year to be better than the previous one, Wipro expects the June 2014 quarter to be weak, owing to weakness in the Indian market. However, considering its strong deals kitty, it remains optimistic about a pick-up thereafter.

Nitin Padmanabhan, technology analyst, Espirito Santo Securities, says: “Wipro has been on an efficiency drive for the past three years and the benefits of these efforts are being seen now. Its fixed-priced projects have risen from 47 per cent to 51 per cent through the past year; the utilisation rate has also improved. These, along with higher realisations, are driving the company’s strong margin performance. Today, Wipro is closing far more deals than in the year-ago period.” (IT SCORECARD)

Most analysts might raise their 2014-15 earnings estimates for Wipro and HCL Technologies, following strong margins posted by these companies for the March quarter. “We expect the Wipro stock to open positive on Monday. The Street is likely to upgrade the margins for Wipro,” says Padmanabhan.

Improving deal signing and better operational efficiencies are being reflected in Wipro’s performance. Wipro and Infosys are Padmanabhan’s top picks in the IT sector.

All-round growth in HCL Technologies’ infrastructure management services and core software services drove the company’s strong performance. The company was struggling to grow its software services business for the past few quarters (it posted one-two per cent rise). Growth in this segment picked up only in the December 2013 quarter.

Harit Shah, IT analyst at Nirmal Bang Institutional Equities, says: “We could raise our earnings estimates four-five per cent for HCL Technologies. We believe the software services pick-up is likely to continue and acceleration in this segment will drive a re-rating for HCL Technologies. TCS maintained positive commentary on discretionary spends, has a strong deal pipeline and expects a better 2014-15. Therefore, TCS and HCL Technologies are our top picks among the top IT companies.”

A continuous exodus at the top- and mid-level management, along with weak client spending, led to revenue contraction for Infosys. A portfolio diversified across verticals, service lines and geographies has enabled TCS to continue seeing healthy growth. The company is quick to identify and ramp up new growth areas (digital, expansion in underpenetrated geographies like Japan), which enables it to put future growth drivers in place.

During the March quarter, Infosys, Wipro and HCL Technologies saw their earnings before interest, tax, depreciation and amortisation (Ebitda) margins expand. Infosys’ margins grew due to reduction in selling, general and administrative (SGA) costs. Wipro’s margins improved due to better utilisation and higher proportion of fixed-price projects. While both TCS and HCL Technologies continued to invest in selling and marketing (S&M) activities, the former’s margins contracted due to weak realisation.

“Margin expansion at HCL Technologies is because of operational efficiencies. A large part of the SGA savings has come more on general and administration costs side, not on the S&M side. We would like to see the company spend more on S&M in the coming quarters. Margins appear at their peak and could move downwards to 25.5-26 per cent,” says Harit Shah.

At Thursday’s closing prices, TCS was trading at 20.2 times its 2014-15 estimated earnings, a premium to the other three companies. Infosys, Wipro and HCL Technologies traded at 15.3 times, 16.6 times and 14.8 times their 2014-15 estimated earnings, respectively. Infosys’ valuations will pick up only when it starts delivering consistent financial performances which, analysts say, could take another 10-12 months. The HCL Technologies stock could witness some re-rating if it continues (or accelerates) the growth in its software services business.

TCS could continue to command a premium over its peers, given its sustained growth performance. However, the company’s current valuations cap significant upsides and have limited room for any negative news flow. Though most analysts are positive on the IT sector, TCS and HCL Technologies are the top picks of most, given their superior performances compared to those of Infosys and Wipro.