"UPI's value grew 700% in 2018 while total digital payments fell 1%")

While digital payments saw a spike post demonetisation, the pace of adoption has been much slower than anticipated. The digital transactions only inched forward in the past year but Unified Payments Interface (UPI), country’s flagship payments platform, is a shining exception.

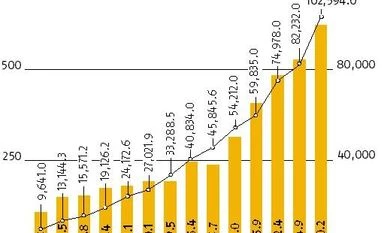

UPI crossed the Rs one trillion milestone for monthly value in December, growing nearly eight times over the previous year. It also achieved a monthly volume of over 600 million, four times the volume of UPI transactions in December 2017, according to data released by National Payments Corporation of India (NPCI).

The total payments industry saw a rise of 27 per cent in volume and a fall of one per cent in November 2018 over November 2017, according to data released by the Reserve Bank of India. The forms of payment include cards, mobile wallets and mobile banking and the data for these forms of payments is only available till November 2018.

Card transaction saw a growth of 22 per cent in volume and18 per cent in value in November 2018 against November 2017. During the same period, wallets grew 86%in volume and 72 per cent in value while UPI grew 400 per cent and 753 per cent respectively.

UPI is a fairly new player in the payments space with a little over two year since its introduction. It was launched in August 2016 with 21 partner banks and saw a monthly transaction volume less than a lakh and value of Rs 3 crore respectively. The platform has seen strong growth ever since then.

NPCI attributes UPI’s success to three main features - simple, seamless and secure, which deliver to the needs of the consumer, merchants, banks and FinTech players.

“UPI was a game-changer in the true sense with complete interoperability being driven on the front end using a mobile phone , with reduced friction while on-boarding and secured two-factor authentication,” said NPCI in response to an email query.

According to Mahesh Makhija, Leader - Emerging Technologies, EY India, UPI is cost-efficient and asset-light compared to other alternatives and in most cases, it can be activated by the recipient (merchant or business) on a self-serve model.

UPI infrastructure was given a further boost with the entry of global majors like Google (Google Pay) and Facebook (Whatsapp Pay). Madhivanan said that these companies brought in not only newer technology but also enormous velocity and cashbacks.

UPI has already overtaken wallets in terms of volume and UPI has nearly twice the monthly volume than e-wallets. UPI is expected to see a major boost in both volume and value of transactions with the introduction of new features in the form of UPI 2.0.

UPI 2.0 will push up the average value of transactions by pushing merchant transactions, say experts.

According to Navtej Singh, chief executive,Digital Business, Hitachi Payment Services, peer to peer transactions continue to dominate UPI volumes but merchant transactions are starting to pick up.“UPI 2.0 extended the feature of overdraft facility and bridged the gap between merchants and customers making UPI a more holistic solution,” he added.

UPI 2.0 is set to roll out its features like Overdraft facility, One Time Mandate, Invoice in the Inbox, Signed intent and QR. This will offer a huge canvas for Banks and Fintechs to collaborate and deliver value to consumers, said NPCI.

“The biggest disruptor is the one-time mandate feature. It can make the payment experience much more seamless, and at the same time give greater control to the customer,” said Kalpesh Mehta, Partner, Deloitte India.

Mehta said that the one time mandate can enable multiple use cases which can help proliferate its adoption. “The only challenge being that its set-up and understanding its features will possibly be limited to digitally savvy smartphone users,” he added.

Last year, foreign payment providers had to face regulatory roadblocks like data localisation. The Supreme Court’s Aadhar judgement has left wallet companies hanging with no means to electronically verify customer documents or onboard new customers. The government’s heavy support for UPI, however, protects it from such threats.

In October, the RBI issued wallet interoperability guidelines though UPI network, enabling wallet companies to have direct access to the UPI network. Previously, they had to use a bank to access the network.

NPCI believes that wallet interoperability should pave the way for increase in the digital transactions and adoption. “While member banks have been building up the supply side through acquisition of merchants, the supply side opens up in a big way through wallet interoperability.”

NPCI said that UPI 2.0 shall see incremental growth coming in through the mandate by SEBI for IPOs to move completely to UPI in a phased manner. “Likewise the various other enhancements, features encompassed in the UPI 2.0 shall provide the ground for future growth,” it added.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in