"Bad loan crisis shows signs of subsiding, say analysts")

Bankers and analysts are finally arriving at a consensus of sorts on the state of non-performing assets in 2017-18.

Bankers say fiscal 2018 would be much better in terms of asset quality than fiscal 2017. Analysts say bad debt accretion would continue in the current fiscal, too, but the numbers may not see the kind of shocking jumps as seen in the fiscal year gone by.

The Reserve Bank of India (RBI) had forced banks to recognise their bad debts between August and March 2017 under an asset quality review. It showed that banks were revealing only a part of the bad assets’ problem. Since then, many banks have created their “watch list” or “drill-down list” for accounts reflecting stress and showing possibilities of going bad.

Gross bad debt in the banking industry as on December was about Rs 7 lakh crore. Adding restructured assets of Rs 2.5 lakh crore, the amount of stressed assets near Rs 10 lakh crore.

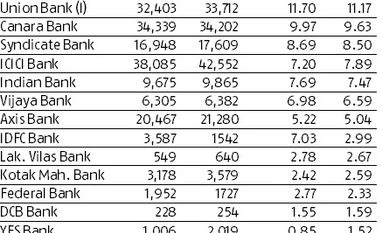

Of all 38 listed banks, 18 have reported their March quarter results. All major private sector banks have reported fourth quarter results, which mostly show a marginal increase in gross non-performing assets (NPA) as a percentage of loans.

According to a CARE Research report, nine private sector banks had a gross NPA ratio of 3.91 per cent, stable from the December quarter’s 3.91 per cent. “It seems that these private sector banks may have reached a stage where they have completed the process of recognising the non-performing assets,” it adds.

FY18 would still be challenging for banks, says Siddharth Purohit of Angel Broking Ltd. “NPA accretion would continue to happen, but the market expects NPAs to come mostly from the watch list. It would be disappointing if fresh slippages come from new loans. Overall, the trend should show incremental slippage are under control.”

Independent analyst Dipankar Choudhury says a lot of what bank management claim about asset qualities and other parameters are with embellishments. “They do it every year. The assessment is not really based on any granular analysis of the portfolio.”

But Choudhury points out that transparency has increased considerably after the asset quality review. Besides, most bad debts were caused by assets acquired during the economic boom. Those assets have run their course. Therefore, the pressure of NPAs subsides on that count, he adds.

Most analysts, though, are not hopeful of a quick turnaround despite the measures taken by the government and the RBI.

According to Moody’s, the recent ordinance and RBI’s action on joint lenders’ forum are credit positive. But they don’t solve key structural issues. This, in part, is an addition to the long list of measures taken by the regulator to resolve the banking system’s bad debt problem.

Analysts say it is unlikely that the recovery mechanism will improve substantially this year, but credit growth may pick up and this would bring down the share of bad loans, as a percentage.

Yearly credit growth is about five per cent. But ICICI Securities expects credit growth to pick up substantially to 10 per cent in FY18 and 14 per cent in FY19.

“As the spreads between bond and loan narrows, there is also an inclination for incremental borrowings in the form of loans, in a falling interest rate environment. With lending rates continuing to decline, retail loan growth is estimated to be higher than systemic loan growth, especially in the mortgage segment. Furthermore, with current inflationary expectations, coupled with improvement in the macro economy, we estimate corporate loans to grow marginally in FY19, taking the systemic loan growth to 14 per cent YoY,” ICICI Securities adds.

This rise in credit, and some control over fresh slippages, should, be able to project bank NPAs at a lower level in percentage terms, adds analysts.

Bankers say fiscal 2018 would be much better in terms of asset quality than fiscal 2017. Analysts say bad debt accretion would continue in the current fiscal, too, but the numbers may not see the kind of shocking jumps as seen in the fiscal year gone by.

The Reserve Bank of India (RBI) had forced banks to recognise their bad debts between August and March 2017 under an asset quality review. It showed that banks were revealing only a part of the bad assets’ problem. Since then, many banks have created their “watch list” or “drill-down list” for accounts reflecting stress and showing possibilities of going bad.

Gross bad debt in the banking industry as on December was about Rs 7 lakh crore. Adding restructured assets of Rs 2.5 lakh crore, the amount of stressed assets near Rs 10 lakh crore.

Of all 38 listed banks, 18 have reported their March quarter results. All major private sector banks have reported fourth quarter results, which mostly show a marginal increase in gross non-performing assets (NPA) as a percentage of loans.

According to a CARE Research report, nine private sector banks had a gross NPA ratio of 3.91 per cent, stable from the December quarter’s 3.91 per cent. “It seems that these private sector banks may have reached a stage where they have completed the process of recognising the non-performing assets,” it adds.

FY18 would still be challenging for banks, says Siddharth Purohit of Angel Broking Ltd. “NPA accretion would continue to happen, but the market expects NPAs to come mostly from the watch list. It would be disappointing if fresh slippages come from new loans. Overall, the trend should show incremental slippage are under control.”

Independent analyst Dipankar Choudhury says a lot of what bank management claim about asset qualities and other parameters are with embellishments. “They do it every year. The assessment is not really based on any granular analysis of the portfolio.”

But Choudhury points out that transparency has increased considerably after the asset quality review. Besides, most bad debts were caused by assets acquired during the economic boom. Those assets have run their course. Therefore, the pressure of NPAs subsides on that count, he adds.

Most analysts, though, are not hopeful of a quick turnaround despite the measures taken by the government and the RBI.

According to Moody’s, the recent ordinance and RBI’s action on joint lenders’ forum are credit positive. But they don’t solve key structural issues. This, in part, is an addition to the long list of measures taken by the regulator to resolve the banking system’s bad debt problem.

Analysts say it is unlikely that the recovery mechanism will improve substantially this year, but credit growth may pick up and this would bring down the share of bad loans, as a percentage.

Yearly credit growth is about five per cent. But ICICI Securities expects credit growth to pick up substantially to 10 per cent in FY18 and 14 per cent in FY19.

“As the spreads between bond and loan narrows, there is also an inclination for incremental borrowings in the form of loans, in a falling interest rate environment. With lending rates continuing to decline, retail loan growth is estimated to be higher than systemic loan growth, especially in the mortgage segment. Furthermore, with current inflationary expectations, coupled with improvement in the macro economy, we estimate corporate loans to grow marginally in FY19, taking the systemic loan growth to 14 per cent YoY,” ICICI Securities adds.

This rise in credit, and some control over fresh slippages, should, be able to project bank NPAs at a lower level in percentage terms, adds analysts.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in