"Few takers for simple tax for small businesses: A look at Composition Scheme under GST")

The introduction of the Goods and Services Tax (GST) has led to a sea change in the taxability of supplies and procedure/compliances to be followed by assessees. GST has also introduced a scheme for the benefit of small businesses called the Composition Scheme.

The Composition Scheme is not alien to India as it was also present in the now-discontinued VAT regime. This scheme has been mainly introduced to help small businesses run smoothly and reduce the compliance burden on them. The supplier is provided with the option of paying an amount calculated at a prescribed rate of the turnover in a state or Union territory (rate of tax has been mentioned in the table) in lieu of the tax to be paid by him.

The objective of the Composition Scheme is to bring in simplicity and to reduce the compliance cost for small taxpayers. To a large extent, the scheme does this by reducing compliances (quarterly returns and payment of taxes prescribed, as against monthly compliances for regular suppliers) and ensuring simplification in taxability (no requirement to determine tax rates/taxability for each product separately), etc.

Below are the key conditions and procedures/compliances that are to be fulfilled by a supplier opting for the Composition Scheme.

1. The persons who are eligible to opt for the Composition Scheme are as follows:

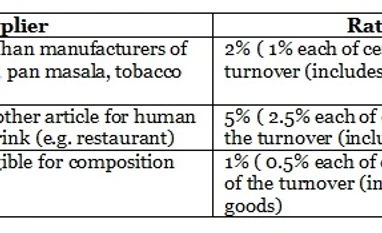

a. The supplier is a manufacturer (except manufacturer of ice cream/edible ice, pan masala, and tobacco) or a trader of goods or is engaged in restaurant services — the supply of food or any other article for human consumption or any drink (other than alcoholic liquor for human consumption).

b. Aggregate turnover* (on an all-India basis) in the preceding financial year does not exceed Rs 50 lakh (in Arunachal, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, and HP) and Rs 75 lakh (in other states/Union Territories).

*Aggregate turnover to include all India turnover of taxable supplies and exempt supplies.

2. The following suppliers cannot opt for the Composition Scheme, irrespective of their turnover:

a. Supplier of services (other than restaurant services mentioned above)

b. A casual or a non-resident taxable person

c. Supplier engaged in supply of goods on which GST is not levied (products not subsumed under GST such as petroleum crude, alcohol, etc)

d. Supplier engaged in inter-state supplies of goods or supply of goods through e-commerce operators (who are required to collect tax at source)

e. A manufacturer of ice cream/other edible ice, pan masala, and tobacco

f. Supplier who has purchased any goods or services from unregistered supplier, unless the supplier has paid GST on such goods or services, on reverse charge basis

3. The key conditions, procedures, and compliances to be followed by a supplier who has opted for the scheme are as follows:

a. The supplier has to file an intimation with the authorities opting for payment of tax under the Composition Scheme along with details of stock. (Relevant forms: Form GST CMP-01, 02 or 03 or ITC-03).

b. The supplier cannot collect the tax from the recipient. Bill of supply issued by the supplier to specifically mention the words "composition taxable person, not eligible to collect tax on supplies" at the top of the bill.

c. The supplier will not be entitled to any credit of input tax paid on procurement of inputs, input services or capital goods.

d. In the case of a supplier migrating to the Composition Scheme from the appointed date ie, July 01, 2017, the supplier should not be holding any stock that is imported or purchased/received from outside the state (including stock transfer).

e. It is mandatory for all locations (across India) of the registered person to opt for the Composition Scheme. The scheme cannot be opted for in isolation for a single location.

f. Supplier shall mention the words "composition taxable person" on every notice or signboard displayed at a prominent place at every place of business.

g. Supplier shall file quarterly returns and make quarterly tax payments by the 18th of the month succeeding the quarter (Relevant return: GSTR-4).

Under GST, there is no restriction for composition dealers to carry out inter-state procurements (as was the case under the erstwhile regime of VAT). One point of caution is that at any given point in time if the supplier does not meet any of the aforementioned conditions or crosses the prescribed thresholds, the supplier would cease to be a composition dealer and would have to start levying applicable taxes at the rates prescribed to normal suppliers.

The Composition Scheme should encourage a lot of small businesses to register under the scheme and pay tax at a fixed rate (highlighted in the table). We are sure that any small issues that suppliers come across would be ironed out in due course.

Rate of tax under the scheme:

Rate of tax under the scheme:

By Pramod Banthia, partner, and Feneel Shah, associate director – indirect tax, at PwC India. Views expressed are personal

Yogesh K Shah, assistant manager – indirect tax PwC, also contributed to this article

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in