"Four years of Modi govt: Market return improves but still below UPA's")

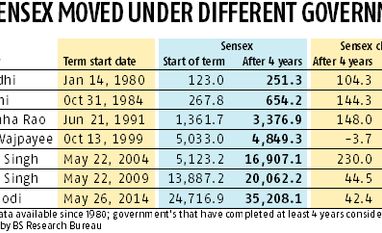

The benchmark Sensex has delivered 42 per cent return in the four years of the Bharatiya Janata Party (BJP)-led National Democratic Alliance (NDA). The returns are slightly below the previous government—Congress-led United Progressive Alliance (UPA), when Sensex had gone up nearly 45 per cent.

Among the seven governments, to have competed four years, this is the second-worst return. The worst returns were under the Atal Bihari Vajpayee-led NDA government, which had assumed office in October 1999. The fallout of the Asian crisis and sanctions imposed following the nuclear test by the Vajpayee government had weighed on the market performance, with the Sensex returning negative four per cent return during the first four years of NDA-I.

The returns for the NDA-II government have been much favorable, thanks a 28 per cent jump in benchmark indices last year. The Sensex was up just six per cent at the half-way mark (first 30 months) for the Modi-government during November 2016. Bouncing off from post-demonetisation lows of 25,807, the Sensex has returned 36 per cent in the past 15 months.

These gain, however, have come on the back of valuation expansion due to lack of corporate earnings growth. Since 2014-15, earnings delivery of India Inc has been muted due to tepid economic growth and the market has consistently traded above its historical average.

“As a result of the weak earnings growth, much of the market upside has been earned through a multiple re-rating– especially in the 2014/15 period (post the election of the NDA government). The sharp rally in 2017 was also due to a significant increase in multiples; with increases in earnings expectations contributing to less than half of total market returns,” says a recent note by Bank of America Merrill Lynch.

At the start of every fiscal, analysts have been forecasting high-teen earnings growth only to be disappointed each time.

Despite the economic boon in form of low oil prices, growth has been sluggish due to policy measures such as demonetisation, implementation of the unified tax regime (GST) and cleanup of the banking sector. Slower economic growth and lack of private investments has taken a tool on corporate earnings growth.

When India was beginning to see improvement in economic and earnings growth, it has been hit by fresh headwind in the form of surging oil prices and weakening of the domestic currency.

“Rising oil prices risk reversing the improving economic fundamental ‘sweet spot’ experienced during 2014-16, at a time when there are heightened market concerns over pre-election populist government policies, the costs of cleaning up the banking sector and the lack of progress in rejuvenating private investment,” says Nomura.

Since 2014, many foreign investors had backed India as biggest overweight in the emerging market (EM) pack given the high growth potential. However, there are now beginning to cut their overweight stance in favour of other markets China, Brazil and South Africa which have demonstrated earnings growth. This has resulted in moderation of foreign portfolio flows (FPIs) into the Indian market.

The government’s decision to re-introduce tax on long-term capital gains (LTCG) and on dividend income is seen as weighing on investor sentiment, The slowdown in FPI flows, however, has been offset by strong investments by mutual funds (MFs). Equity MFs have been flush with capital amid shift in investor preference from debt to equities due to falling interest rates.

With less than year before the next General Elections, topping the UPA-II government in terms of market returns could be a herculean tax for the Modi government. The Sensex had returned 78 per cent in the five years of UPA-II. Most analysts are forecasting the market to remain flat in the next one year amid tightening of interest rates by global central banks, particularly the US Federal Reserve.

In last year of UPA-II, the Sensex had jumped 34 per cent. Nearly half of these gains were on account of optimism that Modi would win the 2014 elections. Also, the market had seen a sharp up move after the BJP bagged strongest mandate in 30 years. The Street was hoping that the huge mandate would spur economic growth by reversing the policy inertia seen in the last leg of UPA-II government amid corruption scandals. However, some believe the government squandered the opportunity.

“Both the economy and markets have been disappointing under this government. Just having a mandate is not good enough,” says Shankar Sharma, vice-chairman and joint managing director, First Global. “India needs a coalition more than a majority government. I think the government runs better when we have a coalition. There are more checks and balances; there is more focus on decision making. The data doesn’t say that India does better in a majority.”

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in