"Economists expect GVA to grow higher at 6.3-6.5% in Q1FY18")

After slumping to a low of 5.6 per cent in the fourth quarter (Q4) of the previous financial year (FY17), gross value added (GVA) is expected to grow around 6.3-6.5 per cent in the first quarter (Q1) of FY18, say economists.

Agriculture and government spending will remain the principal drivers of growth, with industrial growth continuing to be sluggish. The downside risks to this forecast stem largely from the performance of the financial sector.

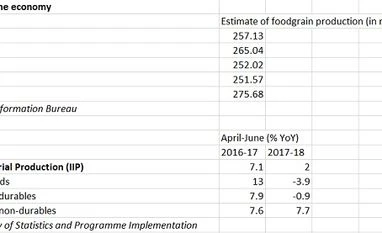

After two years of back-to-back droughts, a normal monsoon has boosted foodgrain production in the country. The fourth Advance Estimates of crop production released on Wednesday showed that overall foodgrain production rose to a record high of 275.68 million tonnes (mt) in 2016-17 (crop year ended in June), up from 251.57 mt last year. This increase will show up in the Q1 agricultural numbers.

“On the back of a healthy rabi outturn assessed by the fourth Advance Estimates of crop production, Icra expects the growth of agriculture, forestry and fishing to improve to 4 per cent in Q1FY18, from 2.5 per cent in Q1FY17,” says Aditi Nayar, principal economist at Icra. Devendra Pant, chief economist at India Ratings, expects agriculture to grow at 3.2 per cent in Q1FY18.

The economy will also benefit from a sharp increase in government spending in Q1.

Following the front-loading of spending, a consequence of the early presentation of the Budget, the central government’s non-interest revenue expenditure has expanded by 26.8 per cent in Q1FY18. It’s capital expenditure, excluding loans disbursed, has grown by a staggering 105.5 per cent in Q1.

Similar to the scenario in Q4 of the previous financial year, strong agricultural growth, coupled with higher government spending, will shore up growth.

“Growth in Q1 will be driven predominantly by agriculture and government spending,” says Suvodeep Rakshit, economist at Kotak Institutional Equities. Other economists like Pant concur.

But industrial growth will continue to be sluggish.

The Index of Industrial Production (IIP) grew by a mere 2 per cent in Q1FY18, down from 7.1 per cent over the same period last year. Within the IIP, the capital goods segment has actually contracted by 3.9 per cent in Q1FY18. It had grown by 13 per cent last year. Similarly, consumer durables - a reflection of demand - have contracted by 0.9 per cent in Q1. It had grown by 7.9 per cent over the same period last year.

Presumably, the disruption to production schedules and discounts offered ahead of the implementation of the goods and services tax (GST) would have weighed down growth.

“The IIP indicates that volume growth in the manufacturing sector moderated sharply to 1.8 per cent in Q1FY18 from 6.6 per cent in Q1FY17, reflecting an effort to shrink inventories ahead of the transition to the GST. Moreover, discounts offered to reduce inventories ahead of the GST would have weighed upon earnings growth in that quarter,” says Nayar. Icra has estimated industry to grow at a mere 3.9 per cent in Q1FY18, down from 7.4 per cent the previous year.

“Manufacturing will be down,” says Pronab Sen, former chief statistician of India, though he adds that given the lack of data, it’s difficult to know how the small and medium enterprises managed have to cope up with the shift to the GST.

While Pant expects the aggregate GVA (in Q1) to grow at 6.4 per cent, Nayar expects it to be marginally lower at 6.3 per cent; the performance of the financial, real estate and professional services sector may pose the biggest risk to this forecast.

After demonetisation, the sector’s growth had plummeted to 3.3 per cent in the third quarter and further to 2.2 per cent in Q4FY17. Now, data from CARE Ratings show that both credit and deposit growth have contracted from April to July this year. How this impacts GVA by the sector will determine whether growth ends up being lower than these forecasts or not.

Source: Press Information Bureau; Source: Ministry of Statistics and Programme Implementation

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in