"Microfinancing lessons from a mandi that govt-run Mudra seems to have lost")

A keen officer in the PMO had asked the finance ministry team that had gone there with the proposal for setting up Mudra, the refinancing agency for micro finance institutions (MFI), what the new solution they hoped to offer for an old problem was. The answer wasn’t particularly brilliant, but the government went ahead nevertheless to set up the agency as a subsidiary of Small Industries Development Bank of India. That was in 2015.

Once India, particularly its rural areas, begins to collect itself from the ravages of the second and third wave of Covid, micro finance is what millions of families will need to turn to. This is where the role of Mudra comes in. Unfortunately, Micro Units Development and Refinance Agency, to give its full name, may not prove to be very helpful. In FY20, the subsidiary of Small Industries Development Bank of India earned nearly half its income of Rs 1,111.9 crore from investments in government paper. In other words, the company copies what many Indian public sector banks do--lend money to the debt market instead of giving out credit. (see table)

Data shows Mudra loans have grown only 5 per cent in FY20, year on year. It does not even cover the nominal rate of growth of the economy. Over 88 per cent of these loans are for the smallest ticket size of Rs 50,000 per borrower known as Shishu loans. In terms of volume Shishu loans were close to half the total loans given out by the company. These are attractive because of their low size and have grown 15 per cent in FY20 over FY19. The universe of larger loans has shrunk.

This means when MFIs take out loans from Mudra, those cover only the puny ones. An out-of-pocket expense for the average Covid bill comes upwards of Rs 40,000. This means any one with a modestly larger need will get a loan at a much higher cost, since those shall be financed from bank money.

No wonder, according to the MicroFinance Institutions Network, of the Rs 2.32 trillion MFI loans, over half came from banks and NBFCs. This is despite Jan Dhan, the no-frills bank accounts that have helped create a robust digital financial services environmentm increasing the proportion of those above the age of 15 with a bank account to nearly 80 per cent in 2017, compared to just about 35 per cent in 2011, notes an NCAER report.

But the same report notes there are “many first-time users and don’t trust unfamiliar ways of handling their money”. This is where MFIs with their soft touch come in most useful to wean them into the formal credit structure. A Business Standard report notes that MFIs like Cashpor Micro Credit have begun to use credit analytics tools to offer “targeted financial services to the underbanked and unbanked population”.

Stress in the MFI sector in the course of post Covid reconstruction allied with Mudra’s AWOL role can be therefore traumatic for the 58 million people across India who depend on MFI loans. Small loans at affordable rates are about the only support the medically wrung-dry families in rural and semi rural areas can now hope to cling on, since cash dole is not likely to be forthcoming from the government.

Beyond Mudra:

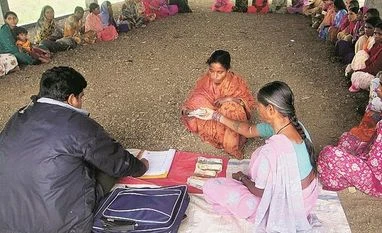

Many vendors at Digha, the largest vegetable open air market in Bihar, take MFI loans to run their business. The plan is simple enough. At Parmanandpur in Vaishali district, MFI agents hand out cash with a small lecture on vaccines to the women. These women take out 15-day loans which they would otherwise source from the money lenders to buy vegetables in bulk to sell at the market, next to the Ganga. The demand is increasing, even in the lockdown, says Gyan Mohan. To service those the industry needs cheap money.

When the industry body for the micro-finance institutions, Sa-dhan wrote to RBI last week to expand their credit window, they were not banking on Mudra jumping in, shaking off its lethargy.

Instead they have their hopes built on the banks and private sector non-banking financial companies. MFIs are hoping they shall get the loans on easier terms so they can in turn provide succour to rural India. Sa-Dhan has asked for a loan forbearance from banks and non-banking finance companies from six months to one year. “During the first wave of Covid, only 40 per cent of these lenders provided a moratorium to us leading to severe liquidity crunch for MFIs”, said P Satish, executive director of Sa-dhan.

One of the largest MFIs in Bihar recognised by the RBI is Adi Chitragupta Finance Limited, based in Patna. Gyan Mohan, CEO and Director of Adi Chitragupta says the agents who disburse the loans are also local boys and girls. So they have a strong understanding of the needs of the rural population.

RBI rules do not say at what rate banks should lend to MFIs but the micro borrowers cannot offer a loan at more than 2.75 times the average base rate of five largest banks. Since banks will not give loans to a MFI at base rate, (it is usually close to 16 per cent), the latter have very less than 500 basis points spread to cover all their costs. Gyan Mohan says the ceiling means MFIs are most reluctant to expand their operations. “If Mudra or Nabard could lend us directly, the rates shall be softer”, he said. The risk premium charged by the banks and NBFCs push up the rates for the sector.

One of the things MFIs do not want is debt waiver. “As the RBI Governor said, a loan waiver hits our collection efficiencies. If a bank is allowed to waive loans, the MFIs will have to follow the same dangerous path”, said Satish. Already Icra reports a reduction in collections and the recovery of loans by the MFIs. There could be a sequential drop of upto 10 per cent in collections in April 2021, which could dip further if Covid cases continue rising and more restrictions are imposed.

Those on the ground are more hopeful. “People are putting on more masks, even if it is often the end of the saree wrapped around their face for women, and are willing to get check ups done for signs of fever”, said Shubham Vineet, Vice President (operations) at AFCL.

INDIA'S MICROFINANCE SECTOR

- Almost 99% microfinance loans in India go to women.

- Most loans provided to joint groups of customers insuring against the risks of defaults.

- Microfinance loans are collateral free. Ticket sizes can be up to Rs 125,000, with average ticket sizes being around Rs 36,000.

- Lenders include Banks, Small Finance Banks, NBFC-MFIs, NBFCs.

- The industry has an outreach in almost 600 districts of India. In terms of geographic spread, 76% of the loan portfolio is rural and 24% urban.

- Interest rate of NBFC-MFIs is regulated by the RBI. Overall interest rate charged to the customer range between 18-24%.

Table: A quick look at India's microfinance space

| Mudra particulars | 2019-20 (Rs cr) | 2018−19 (Rs cr) |

| Revenue from operations | 616.51 | 574.32 |

| Other income | 495.39 | 286.61 |

| Total income | 1,111.90 | 860.93 |

| Industry overview | ||

| MFI portfolio as on December 2020 | Rs 2,32,648 crore* | |

| Number of borrowers | 58.3 million | |

| * Of this, as on... | March 2020 | March 2019 |

| NBFC | 22,702 | 20,191 |

| Small finance banks | 40,556 | 30,322 |

| banks | 92,281 | 59,897 |

| NBFC-MFIs | 73,792 | 67,009 |

| Total | 231,788 | 179,314 |

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in