"MPC's dilemma: Inflation down but pulses could pose a problem")

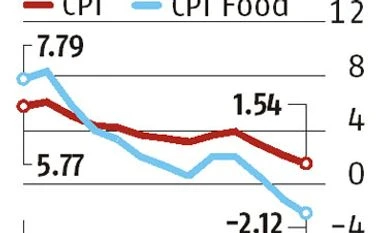

Headline inflation dipped to 1.5 per cent in June, well below the lower end of the Reserve Bank of India (RBI)’s inflation target of 4 plus-minus 2 per cent. Industrial activity continues to remain sluggish. Yet is there a case for maintaining the status quo on interest rates, when the RBI’s monetary policy panel (MPC) announces its policy stance on Wednesday?

In recent months, retail inflation has consistently undershot the RBI’s forecasts. Much of this decline in inflation was driven by falling food prices, particularly those of pulses and vegetables. The former fell by 21.9 per cent in June, while the latter declined 16.53 per cent. But some experts say there is a growing risk that this trend may not continue in the coming months.

Take the case of pulses.

The decline on the pulses index in the Consumer Price Index (CPI) has been driven largely by four items — arhar, moong, masur and urad. These together account for 72 per cent of the pulses index. Prices of these items fell 29.6 per cent in June, while those of other items actually rose 3.5 per cent. But will this downward trend continue?

Crop sowing data as on July 28, 2017, show that area under pulse cultivation stood at 11.5 million hectares, up from 10.7 million last year. But a detailed break-up shows that area under arhar cultivation has fallen to 3.5 million hectares, from 4.1 million hectares the year before. This could lead to a shortfall in production, pushing up prices. Arhar alone accounts for a third of the pulses index.

“It’s the cobweb syndrome,” says Madan Sabnavis, chief economist at CARE. “Cropping decisions tend to be based on previous year’s prices.”

So, a fall in prices of a crop over the last year would prompt farmers to shift to other crops, reducing area under cultivation of some. This would reduce production and raise prices. Crop sowing data show such a move is already underway.

Cotton sowing has averaged about 20 per cent over the past two weeks, up from 5.6 per cent before that, according to a report by Morgan Stanley, “likely reflecting a shift away from rain-fed crops like pulses and oilseeds towards cotton sowing.” This could lead to higher prices in the coming months. But the extent of its impact on pushing up inflation is debatable.

“While arhar sowing is lagging last year’s level, the average retail price remains a fraction of the July 2016 level,” says Aditi Nayar, principal economist at ICRA.

Devendra Pant, chief economist at Ind-Ra, says: “The base effect will start wearing off around October. But food prices are low. So even if there is a reversal in prices, the impact on the index may still be muted.”

But others like Pronab Sen, former chief statistician of India, say that as global pulses market is very thin, shortages could lead to price spikes.

The MPC is believed to be worried about pulse inflation rearing its ugly head. Add to this the recent surge in tomato prices, and the outlook for inflation looks muddled.

Tomato prices, which were contracting since September last year, jumped 40.3 per cent in July over last year, according to Ministry of Consumer Affairs’ data. On a month-on-month basis, these have risen 166 per cent.

“Average tomato price in July 2017 has spiked on a sequential basis, and exceeded the level for July 2016, which may infuse some caution in the MPC’s outlook for inflation and future rate cuts,” says Nayar. Tomato has a weight of 9.5 per cent in the vegetable index.

“The recent twist has been on account of vegetable prices,” says Sabnavis. “One or two items can reverse the downward trend in inflation. I expect the MPC to hold rates, even though it is tempting as inflation is below 2 per cent. By October we will give a better picture.”

Others say a split verdict cannot be ruled out, but with more members voting for a cut.

“The MPC’s decision is unlikely to be unanimous, as some members may choose to focus on the expected rise in CPI inflation after August 2017 rather than the lower-than-expected prints over the last several months,” says Nayar. “Overall, the balance is tilted towards a 25-basis point repo rate cut in the next bi-monthly meeting.”

Soumya Kanti Ghosh, group chief economic advisor, SBI, says in a report: “Our bet of the odds of a rate decision (preferably cut) this time could be 4-2.”

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in