"Realty sector still reeling from after effects of note ban: Economic Survey")

The sting of demonetisation is still hurting the real estate and housing sector, which is in the doldrums. From hitting a five-year low in residential property sales in the top eight cities, a measly 1.7 per cent growth in the construction sector last year as compared to five per cent in 2015-16, to challenges such as approvals of permits, rising debt levels and non-performing assets (NPAs), the second part of the Economic Survey of 2016-17 has presented a cautious picture of the sector.

According to the Survey, residential sales across the top eight cities in India fell to a five-year low of about 245,000 units in FY17, due to subdued demand over the past three years. Similarly, new residential unit launches, too, fell to 176,000, a 64 per cent decline. Sales were down by nearly one-third. This was primarily due to the prolonged slump and execution delays in project completion which resulted in inventory pile-up.

“Demonetisation in November last year possibly impacted the new launches and sales in the short-term with several states recording a drop in property registrations post demonetisation. Foreign direct investment (FDI) inflows to the construction sector have also declined to $1.9 billion in 2016-17, as against $4.6 billion in 2015-16, even though there was relaxation of FDI norms for the construction development sector undertaken over the past two to three years,” the Survey said.

According to industry experts, despite several reforms brought in by the government, the industry has seen de-growth for the past several quarters. “While the government has tried a series of reforms in the form of relaxation in FDI norms, enhanced incentives under PMAY, introduction of REITs and enactment of Rera, the impact of these reforms is not visible as of now,” said Neeraj Sharma, director, Grant Thornton Advisory Private Limited.

The Survey also highlighted the longstanding problem faced by real estate developers of getting multiple approvals and points out that by-laws have not been updated according to the global standards.

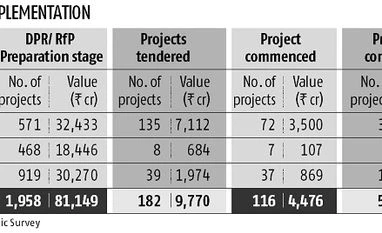

“With over 30–35 regulatory approvals required to be obtained by a developer, it takes anywhere between six to 12 months to just obtain them. The whole process is cumbersome and delays projects, inflating project cost by up to 30 per cent,” the Survey said.

Experts said that while the government has been able to bring in regulatory changes such as introduction of real estate regulatory act (Rera) and the goods and services tax (GST), resources on the ground were not efficient enough to enforce them, leading to much confusion.

“Getting approvals should be efficient, right now it is counter-productive. This is one of the biggest challenges the sector is facing at present. Right now what exactly is happening on the ground is unclear. While the government has taken some great steps, implementation is still a problem,” said Samantak Das, chief economist and national director–Research, Knight Frank India.

The real estate sector has also been grappling with liquidity issues and piling debt.

The total outstanding debt of listed real estate developers in India has risen from Rs 25,000 crore ($3.7 billion) in 2006-07 to over Rs 83,000 crore ($12 billion) in 2015-16.

According to Parveen Jain, real estate body NAREDCO’s president, the de-growth in the sector is going to continue for the next two years before things start looking up.

SMART CITIES SHOULDN’T MERELY BE CONFINED TO DIGITAL TECHNOLOGY

Residential sales across the top eight cities in India fell to a five-year low of about 245,000 units in FY17, due to subdued demand over the past three years.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in