"Sebi may tighten AIF regulations to better monitor the source of funding")

The Securities and Exchange Board of India (Sebi) plans to tighten regulations for Alternative Investment Funds (AIF) to better monitor the source of funding and their end use.

According to sources, Sebi may check anti-money laundering policies implemented by AIFs and examine the sanctity of back-end arrangements that investment vehicles might have with investors. The move is to prevent instances where money raised in AIFs is invested back in entities owned by the investors.

The regulator might also conduct regulatory audits on AIFs to examine fund sourcing arrangements in order to ensure regulations are not violated.

“Sebi might be inclined to monitor the source of funding to ensure the AIF route is not misused, given the wide range of investors from whom the money can be raised and the limited investor base,” said Tejesh Chitlangi, partner, IC Universal Legal.

AIFs can raise money from both domestic and foreign investors. Unlike mutual funds, which can raise overseas money only from foreign portfolio investors (FPIs) and NRIs, AIFs can do so from all classes of overseas investors.

Present AIF regulations contemplate an investment in debt, which has prompted certain funds to extend loans that otherwise cannot be done under the present Sebi and Reserve Bank of India (RBI) norms.

According to sources, Sebi may check anti-money laundering policies implemented by AIFs and examine the sanctity of back-end arrangements that investment vehicles might have with investors. The move is to prevent instances where money raised in AIFs is invested back in entities owned by the investors.

The regulator might also conduct regulatory audits on AIFs to examine fund sourcing arrangements in order to ensure regulations are not violated.

“Sebi might be inclined to monitor the source of funding to ensure the AIF route is not misused, given the wide range of investors from whom the money can be raised and the limited investor base,” said Tejesh Chitlangi, partner, IC Universal Legal.

AIFs can raise money from both domestic and foreign investors. Unlike mutual funds, which can raise overseas money only from foreign portfolio investors (FPIs) and NRIs, AIFs can do so from all classes of overseas investors.

Present AIF regulations contemplate an investment in debt, which has prompted certain funds to extend loans that otherwise cannot be done under the present Sebi and Reserve Bank of India (RBI) norms.

A recent adjudication order passed by a Sebi officer observed that SREI AIF had floated a fund and gave out loans instead of investing in debt securities.

The AIF regulations do not permit disbursal of loans as this would be tantamount to operating a non-banking financial company (NBFC) through the AIF route.

The regulator might look at revising the definition of ‘associate’ under AIF regulations, said sources.

Today, the definition is not aligned with the Companies Act or with the accounting standards and merely states that an entity is an associate if the sponsor or trustee or manager (or any of their respective directors) hold more than 15 per cent in the target investee company. This could change.

“Investment by an AIF in an ‘associate’ requires approval of investors. By aligning the associate’s definition, sponsors or managers will not be able to divert the funds raised to their captive projects or financing requirements,” said Shagoofa Khan, partner, Cyril Amarchand Mangaldas.

An email sent to Sebi did not elicit a response.

The larger issue is how the AIF route could be used to circumvent other laws, said Bombay High Court advocate P R Ramesh. “Related-party transactions, for instance, can be concealed using AIF as pass-through. It may be necessary for making some disclosures public, particularly when paired companies are involved as investor or investee,” he added.

There are other grey areas in the AIF regulations that need to be addressed. According to industry experts, the provision that prohibits venture capital funds from investing in NBFCs still continues and has created practical hardships in today’s era of fintech venture capitalists. Similarly, there is ambiguity regarding the calculation of unlisted versus listed investment portfolio for Category II AIFs.

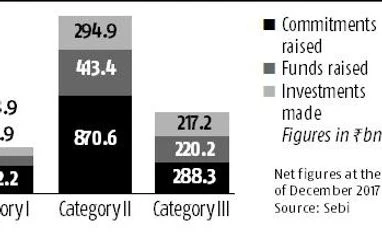

Sebi data showed investment commitments of AIFs reached Rs 1.41 trillion as of December, over four-fold jump from Rs 307 billion two years ago.

The surge in assets is a function of easing regulatory framework, options for customisation and robust returns. Besides providing for a pass-through to category I and II AIFs, the government has effected several other changes in the past three years. For instance, the holding period for availing of long-term capital gains in investments made by AIFs in the unlisted space was reduced to two years from the earlier three years. The one-year lock-in period for AIFs post-initial public offerings has been done away with.

AIFs are privately-pooled investment funds, categorised into three categories. Category I funds invest in start-ups, small and medium-sized enterprises (SMEs) and venture capital. Category II funds include private equity funds and debt funds, while category III includes hedge funds.

The AIF regulations do not permit disbursal of loans as this would be tantamount to operating a non-banking financial company (NBFC) through the AIF route.

The regulator might look at revising the definition of ‘associate’ under AIF regulations, said sources.

Today, the definition is not aligned with the Companies Act or with the accounting standards and merely states that an entity is an associate if the sponsor or trustee or manager (or any of their respective directors) hold more than 15 per cent in the target investee company. This could change.

“Investment by an AIF in an ‘associate’ requires approval of investors. By aligning the associate’s definition, sponsors or managers will not be able to divert the funds raised to their captive projects or financing requirements,” said Shagoofa Khan, partner, Cyril Amarchand Mangaldas.

An email sent to Sebi did not elicit a response.

The larger issue is how the AIF route could be used to circumvent other laws, said Bombay High Court advocate P R Ramesh. “Related-party transactions, for instance, can be concealed using AIF as pass-through. It may be necessary for making some disclosures public, particularly when paired companies are involved as investor or investee,” he added.

There are other grey areas in the AIF regulations that need to be addressed. According to industry experts, the provision that prohibits venture capital funds from investing in NBFCs still continues and has created practical hardships in today’s era of fintech venture capitalists. Similarly, there is ambiguity regarding the calculation of unlisted versus listed investment portfolio for Category II AIFs.

Sebi data showed investment commitments of AIFs reached Rs 1.41 trillion as of December, over four-fold jump from Rs 307 billion two years ago.

The surge in assets is a function of easing regulatory framework, options for customisation and robust returns. Besides providing for a pass-through to category I and II AIFs, the government has effected several other changes in the past three years. For instance, the holding period for availing of long-term capital gains in investments made by AIFs in the unlisted space was reduced to two years from the earlier three years. The one-year lock-in period for AIFs post-initial public offerings has been done away with.

AIFs are privately-pooled investment funds, categorised into three categories. Category I funds invest in start-ups, small and medium-sized enterprises (SMEs) and venture capital. Category II funds include private equity funds and debt funds, while category III includes hedge funds.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in