"Banks to recoup market share as high rates, tighter liquidity hit NBFCs")

The recent rise in interest rates and tighter liquidity in the bond market after the default by Infrastructure Lending & Financial Services (IL&FS) is likely to tilt the balance in favour of banks. A steady decline in 10-year government bond yields beginning the second half of 2014 led to a sharp decline in borrowings costs for non-bank lenders, improving their competitiveness against commercial banks that rely on low-cost deposits.

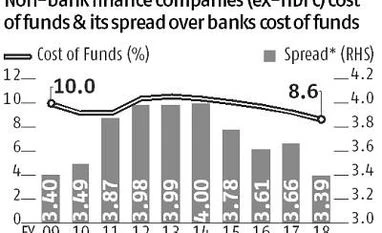

The average cost of borrowings (or cost of funds) for listed retail lenders declined from a high of 10.13 per cent in FY13 to a decade low of 8.21 per cent in FY18. The decline was even sharper for non-bank finance companies (NBFCs), excluding Housing Development Finance Corporation (HDFC), as the cost of funds declined to a decade low of 8.6 per cent (on average) in FY18, from a high of 10.6 per cent in FY13.

As a result, the spread between the cost of funds of NBFCs (ex-HDFC) and of banks declined to a decade low of 3.39 per cent in FY18 on average, from 4 per cent in FY14. In the same period, their margins (excess of yields on advances over cost of funds) expanded to 760 basis points in FY18 from 650 basis points in FY14, on average. In comparison, banks’ margins were stable at around 6.9 per cent during the period.

The analysis is based on the audited finances of listed retail NBFCs that are part of the BSE500 index. The Business Standard sample includes 21 NBFCs. In banks, 37 listed public sector (PSBs) and private lenders were included.

Given its large size and superior balance sheet, HDFC is an outlier in the NBFC space, with cost of funds being closer to banks rather than other non-bank lenders. For example, HDFC’s cost of funds were 116 basis points lower than what other retail NBFCs paid on average, and only 52 basis points higher than banks’ average cost of funds in FY18.

Analysts expect the cycle to shift in favour of banks as the rise in interest rates will push up NBFCs’ borrowings, thus bringing down margins. “Unlike banks, NBFCs largely rely on market borrowings to fund their operations. The rise in yields and tight liquidity conditions will push up their borrowings cost, resulting in lower margins and a slowdown in loan growth," says G Chokkalingam, founder and MD of Equinomics Research & Advisory Services.

.

Analysts now expect banks to recoup some market share loss, thanks to recent developments. "Banks with access to low-cost deposits have a cost advantage over NBFCs in a rising interest rate scenario, but gains will largely flow to large private sector banks that have capital to grow their loan book. Public sector banks with poor capital adequacy may still lose market share," said Dhananjay Sinha, head of research, Emkay Global Financial Services.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in