"Irdai's no to HDFC-Max merger could impact sector valuations")

Max Financial Services' stock has shed about six per cent in the past two trading sessions, after the Insurance Regulatory and Development Authority of India (Irdai) rejected the proposed merger of Max Life Insurance and HDFC Standard Life Insurance.

The grand merger announcement last June had led to significant re-rating in the stocks of their parent companies, HDFC and Max Financial Services. At the time, both stocks were languishing at their 52-week low. News of the merger gave the shares a needed boost on the bourses. These gained 28-41 per cent, with Max Financial hitting its 52-week high before it gave up some gains after reports in mid-May that Irdai would say No.

The contours of the proposed merger had raised questions from the beginning, including payment of a non-compete fee to the promoters of Max Financial. Even so, Irdai's rejection on the basis of the deal structure not being appropriate is interesting. The life insurance business, particularly for listed companies, is modelled on a holding subsidiary structure. So, Irdai's decision practically shuts the door on a reverse merger option — an unlisted company merging with a listed one to enjoy automatic listing.

Listing is a critical progression for HDFC Life. Over the years, the business has matured into a robust model and it is natural for its investors, particularly for Standard Life (holding 35 per cent stake) to capitalise. Reports suggest that with the proposed merger hitting a block, HDFC Life has revived its earlier plan of an initial public offering (IPO) of equity.

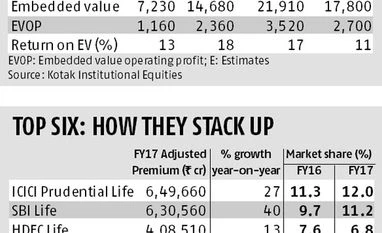

However, with the company in third position in terms of market share and having seen slower growth in FY17 in terms of adjusted premiums (see table), it needs to be seen what investors will be willing to pay for a share. A year before, the combined entity of HDFC Life and Max Life was valued at 3.4 times the FY18 estimate of price to embedded value. Analysts increased the contribution of HDFC Life to HDFC’s overall valuations from about 10 per cent to 13–14 per cent after the merger announcement.

For Max Life, while its FY17 performance was ahead of expectations, the lack of a stable banking channel or bancassurance — as with HDFC Life and HDFC Bank or ICICI Prudential Life and ICICI Bank — remains a concern. While Max Life has partnered with Axis Bank (tie-up valid till FY21) and YES Bank for bancassurance, these require periodic renewal.

An analyst from a foreign brokerage notes that Max Life had seen some senior exits in anticipation of synergy from a HDFC Life merger. “Now, Max Life has to entail additional costs to keep its business going,” he says.

Chances of a rapid progression in market share for HDFC Life and Max Life also become stretched. The merged entity was expected to take top slot among private insurers.

The sector as a whole might have to go back to the drawing board to restructure their holding strategies after Irdai's verdict. “Within the listed space, the life insurance business is usually held as a step-down subsidiary. Promoters looking to monetising the businesses might have to rework their model,” says a lawyer who advises private insurers.

Therefore, the valuations for Aditya Birla Nuvo (holding company of Birla Sun Life), Bajaj Finserv, Exide and Reliance Capital could get moderated with the mega merger not going through in the near-term. These stocks got re-rated by five to 10 per cent, owing to their life insurance exposure, last year.

Even HDFC and Max Financial might see a moderation in valuation. While HDFC has not seen any downside, given the preparations for an IPO, this cannot be said for Max Financial. The analyst quoted above expects a 15–20 per cent downside for the latter. “Much of the stock rally can be credited to the merger. With that going off, buying interest will also recede for Max Financial,” he warns. The fall in the share price backs this view.

However Adarsh Parasrampuria of Nomura says with the merger euphoria fading away, Max Financial’s stock is better placed. “While it is a setback, Max Financial now trades at decent levels,” he says. Alpesh Mehta of Motilal Oswal Financial Services adds that with financial institutions, particularly life insurance, being the biggest beneficiary of demonetisation, Max Financial might do well even without the merger.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in