"Masayoshi Son dials up a wrong number")

Masayoshi Son is a man of grand ambitions. But his dream of raising $30 billion in an initial public offering of his Japanese mobile-phone company may be a stretch.

SoftBank Group Corp. is seeking a valuation of about $90 billion for its domestic wireless business and is speaking to advisers about selling a third of the unit, Giles Turner, Ruth David and Takahiko Hyuga of Bloomberg News reported, citing people familiar with the matter.

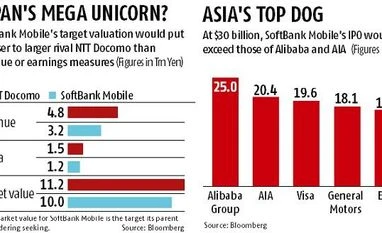

A deal of that size would make SoftBank Mobile the biggest IPO in history, surpassing the $25 billion raised by Jack Ma’s Alibaba Group Holding Ltd. in 2014. It would also render a US offering inevitable. On its own, the Tokyo market could not absorb a sale of that magnitude. Japan’s biggest IPO since the 2000s was the $11.6 billion flotation of Japan Post Holdings Co last year, and that is now trading below its offer price.

The attraction for potential investors in Masa’s Japanese telecoms unit is simple: Yield. The company is a cash cow that delivers around half the parent’s operating income.

At $90 billion, SoftBank Mobile would be valued at close to NTT Docomo Inc, a much larger rival. There are two more reasons, however, why the mooted valuation is crazy.

First, paying so much for yield makes sense only if payouts can keep pace with a rising share price, which is what every investor hopes for when she buys into an IPO.

SoftBank will have its work cut out on that front. Japanese wireless services are a tough industry — and not just because of an aging population. Competition is heating up. E-commerce firm Rakuten Inc is planning to start a wireless operator in Japan with lower network costs than Docomo, SoftBank and KDDI Corp. Three operators are seen as optimal in most markets; a fourth can destroy the industry’s profitability, as any India watcher could tell you.

A second reason why investors should pause is corporate governance. While Masa will be as eager as any shareholders to receive dividends from the unit, there are other means for SoftBank to extract cash from a business that it will continue to control. In March, in preparation for the IPO, the wireless company paid a lump sum of 350 billion yen ($3.1 billion) to its parent for the right to use the SoftBank brand trademark. In effect, SoftBank stripped cash from the telco’s balance sheet and replaced it with what some might deem useless intangible assets.

If investors need any reminder that SoftBank lacks a strong corporate governance track record, just look at how it threw private bank buyers of its dollar bonds under the bus earlier this year.

Ultimately, it’s odd to expect investors to subscribe in such bulk for a yield play. Blockbuster IPOs usually have a growth story to tell — such as Alibaba, which held the promise of capitalising on China’s burgeoning e-commerce appetite.

That’s quite a different pitch from a company that operates in a mature and increasingly competitive industry — and with a founder who hasn’t been shy about using its cash.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in