"Only major firms relishing masala bonds")

Masala bonds, or rupee-denominated bonds issued by Indian firms, have caught the fancy of at least three companies. But these cannot be called a game changer yet, said market observers.

Lower-rated companies, for one, might have little chance to tap the market to raise funds.

The issuers have so far been highly rated but their international ratings are limited by the country’s sovereign rating of BBB-, a shade above junk. The rupee’s recent stability and the high yields of the bonds have added to the attraction, but investors are bearing credit risk, currency risk and rates risk.

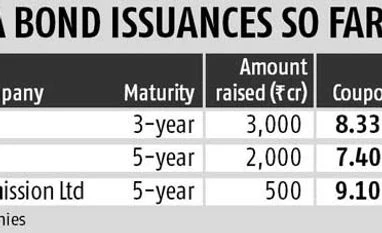

The demand for the papers was phenomenal. The issuers, though big names, raised money at a cost higher than the companies would have raised in the domestic market. Thus, the cost of fund-raising cannot be termed cheaper. The foreign investors had refused to bear the withholding tax and the issuer, on top of the initial coupon, also added the tax component as the final rate of return on these bonds. So far, only three masala bond issuances have taken place. HDFC Ltd was the first in the space; it raised Rs 3,000 crore in July. State-owned NTPC raised Rs 2,000 crore and Adani Transmission raised Rs 500 crore earlier this month. There were talks of HDFC going for a second tranche of bonds in September-October, but the company’s spokesperson did not confirm that.

NTPC managed to raise the bonds at 20 basis points lower than the domestic AAA benchmark, before adjusting for withholding tax that the investor should pay to the government. But for now, the issuers are bearing the cost to make masala bonds popular.

These are highly rated companies and are familiar names to overseas investors. Papers of these companies have huge demand even in the domestic market. By tapping the masala bond market, these companies are helping broad-base the investor base for other Indian firms, which need alternative sources of funding, particularly cheap funding from abroad.

However, for now, the market will be restricted to highly rated firms. “More quality, blue-chip names will be able to tap the initial offshore rupee bond market, as investors can focus risk management on rates and forex rather than worrying about the credit element. Also, given that liquidity is still an issue for investors who are looking to trade the bonds, masala bonds will appeal much more to buy-and-hold investors,” Doshi said. According to Naresh Takkar, Group CEO at ICRA Ltd, lower rated firms will be able to tap the market overtime, but not immediately, as even in the domestic market, the bond route is restricted to higher rated firms. “However, there could be special category of investors looking for higher yields who would be interested in lower rated bonds too,” said Takkar, adding, “the masala bonds market can be a good funding avenue for firms with large funding requirement and are looking to diversify their source of funding for varied reasons, including exposure norms in the local market.”

HDFC’s three-year bonds bore a fixed semi-annual coupon of 7.875 per cent, a rate that would have been possible while raising money onshore. But, compensating for the additional tax the investors would incur, the all-in annualised cost has come to around 8.33 per cent per annum. “Even for a top company, the bonds are not a cost-effective avenue,” said the head of treasury of a foreign bank who did not wish to be named. “The reason for going in to this market is purely the novelty factor for now. Otherwise, it makes very little sense for the companies to offer the withholding tax component every time they issue a bond.”

According to the banker, demand for these bonds will take a long time to get established. Till then, only sporadic issuances can be expected.

Jayesh Mehta, head of treasury at Bank of America-Merrill Lynch, agreed that it will take time to make Masala bonds acceptable to international investors. “Demand for the bonds of lower rated companies will be quite muted. Foreigners ask far more risk premium than Indian investors who are familiar with the Indian names,” Mehta said.

However, government power and utility companies might keep the fire burning as Prime Minister Narendra Modi had promised to list $1-billion equivalent of masala bonds in the UK during his November 2015 visit. But that would be contained within the public sector space.

Bankers advising such issuances said state-owned companies might not increase their borrowing plans for the year, but might curtail domestic market issuances in favour of masala bonds. This will increase demand for the domestic papers.

“NTPC, PFC, REC ... these companies issue bonds of around Rs 20-30,000 crore each every year in the domestic market and the demand for these papers is huge. If masala bonds eat up a portion of these, the demand will shoot up even more. This, perhaps, will offset some of the cost associated with the overseas bonds,” said a banker arranging masala bond issuances for public sector companies.

However, the banker said the initial interest from corporate clients has evaporated after HDFC had to pay the withholding tax component with the coupon.

Lower-rated companies, for one, might have little chance to tap the market to raise funds.

The issuers have so far been highly rated but their international ratings are limited by the country’s sovereign rating of BBB-, a shade above junk. The rupee’s recent stability and the high yields of the bonds have added to the attraction, but investors are bearing credit risk, currency risk and rates risk.

The demand for the papers was phenomenal. The issuers, though big names, raised money at a cost higher than the companies would have raised in the domestic market. Thus, the cost of fund-raising cannot be termed cheaper. The foreign investors had refused to bear the withholding tax and the issuer, on top of the initial coupon, also added the tax component as the final rate of return on these bonds. So far, only three masala bond issuances have taken place. HDFC Ltd was the first in the space; it raised Rs 3,000 crore in July. State-owned NTPC raised Rs 2,000 crore and Adani Transmission raised Rs 500 crore earlier this month. There were talks of HDFC going for a second tranche of bonds in September-October, but the company’s spokesperson did not confirm that.

NTPC managed to raise the bonds at 20 basis points lower than the domestic AAA benchmark, before adjusting for withholding tax that the investor should pay to the government. But for now, the issuers are bearing the cost to make masala bonds popular.

These are highly rated companies and are familiar names to overseas investors. Papers of these companies have huge demand even in the domestic market. By tapping the masala bond market, these companies are helping broad-base the investor base for other Indian firms, which need alternative sources of funding, particularly cheap funding from abroad.

However, for now, the market will be restricted to highly rated firms. “More quality, blue-chip names will be able to tap the initial offshore rupee bond market, as investors can focus risk management on rates and forex rather than worrying about the credit element. Also, given that liquidity is still an issue for investors who are looking to trade the bonds, masala bonds will appeal much more to buy-and-hold investors,” Doshi said. According to Naresh Takkar, Group CEO at ICRA Ltd, lower rated firms will be able to tap the market overtime, but not immediately, as even in the domestic market, the bond route is restricted to higher rated firms. “However, there could be special category of investors looking for higher yields who would be interested in lower rated bonds too,” said Takkar, adding, “the masala bonds market can be a good funding avenue for firms with large funding requirement and are looking to diversify their source of funding for varied reasons, including exposure norms in the local market.”

HDFC’s three-year bonds bore a fixed semi-annual coupon of 7.875 per cent, a rate that would have been possible while raising money onshore. But, compensating for the additional tax the investors would incur, the all-in annualised cost has come to around 8.33 per cent per annum. “Even for a top company, the bonds are not a cost-effective avenue,” said the head of treasury of a foreign bank who did not wish to be named. “The reason for going in to this market is purely the novelty factor for now. Otherwise, it makes very little sense for the companies to offer the withholding tax component every time they issue a bond.”

According to the banker, demand for these bonds will take a long time to get established. Till then, only sporadic issuances can be expected.

Jayesh Mehta, head of treasury at Bank of America-Merrill Lynch, agreed that it will take time to make Masala bonds acceptable to international investors. “Demand for the bonds of lower rated companies will be quite muted. Foreigners ask far more risk premium than Indian investors who are familiar with the Indian names,” Mehta said.

However, government power and utility companies might keep the fire burning as Prime Minister Narendra Modi had promised to list $1-billion equivalent of masala bonds in the UK during his November 2015 visit. But that would be contained within the public sector space.

Bankers advising such issuances said state-owned companies might not increase their borrowing plans for the year, but might curtail domestic market issuances in favour of masala bonds. This will increase demand for the domestic papers.

“NTPC, PFC, REC ... these companies issue bonds of around Rs 20-30,000 crore each every year in the domestic market and the demand for these papers is huge. If masala bonds eat up a portion of these, the demand will shoot up even more. This, perhaps, will offset some of the cost associated with the overseas bonds,” said a banker arranging masala bond issuances for public sector companies.

However, the banker said the initial interest from corporate clients has evaporated after HDFC had to pay the withholding tax component with the coupon.