"RBI's liquidity clean-up to push bond yields")

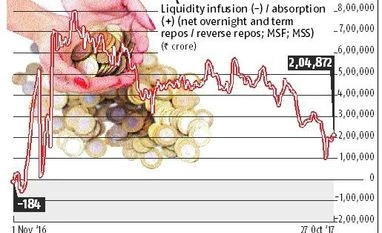

One year after demonetisation was announced, banking system liquidity is still in surplus territory even as the central bank and the government used all that they had in their means to neutralise the surge of deposits in the banking channel.

Only in the Reserve Bank of India’s (RBI’s) liquidity adjustment facility alone, banks parked their surplus liquidity in excess of Rs 5 lakh crore on November 25, 2016, prompting the RBI to announce 100 per cent cash reserve ratio (CRR), from the normal four per cent, for incremental deposit mobilised over a certain period. CRR is the share of deposits banks maintain with the central bank free of cost.

Data compiled by rating agency Icra show at its peak, net absorption of liquidity — through various instruments by the central bank and the government — reached about Rs 8 lakh crore by early January, indicating the extent the banks put their money in the central bank.

The central bank has become more aggressive in its liquidity absorption exercise since then, and has sold Rs 90,000 crore of bonds in the open market to remove excess liquidity. Besides, between December 2, 2016, and March 13, 2017, the government issued cash management bills (CMBs), or specialised short-term treasury bills, issued under the market stabilisation scheme (MSS) to neutralise excess liquidity. At its peak in mid-January, CMB outstanding was worth more than Rs 5 lakh crore.

The daily average liquidity absorption under the liquidity adjustment facility of the RBI declined to Rs 2.74 lakh crore during the second quarter (Q2) of FY18, from Rs 3.52 lakh crore in the first quarter (Q1). Including CMBs and treasury bills issued under MSS, the daily average surplus liquidity eased mildly to Rs 4.38 lakh crore in Q2, from Rs 4.58 lakh crore in Q1, said Icra in a research note.

The reason why it was important to drain excess liquidity was that it would have stoked inflation, which the central bank is fighting to keep under four per cent. However, a surplus liquidity regime also distorts the transmission of the RBI policy rates. In response to the central bank’s cumulative 200-basis points (bps) policy rate cut, bank lending rates have fallen by about 120 bps. One reason cited by banks was that they cannot cut deposit rates drastically even as people continue to park their money. And since deposit rates have not fallen, lending rates cannot fall too, they say.

Draining liquidity would help the central bank get a grip on the situation and direct banks as the situation prevails for an effective transmission.

But, according to Soumyajit Niyogi, associate director of India Ratings and Research, draining liquidity would make it difficult for banks to cut rates. It is a dilemma for the central bank that wants the banks to lower lending rates faster.

Even as deposit growth shot up, credit growth for the most part of last year remained in mid-single digits. Only now, there are some signs that credit growth is picking up. Credit growth is now at 7.5 per cent, whereas deposit growth is 8.7 per cent and growth rates are converging.

As credit and deposits growth converge, liquidity will tighten even further, said Nomura in a report. “We expect this trend of convergence between credit and deposit growth to continue. A cyclical recovery and higher commodity prices should boost working capital needs, while the availability of growth capital after the recently announced recapitalisation plan should also enable public sector banks to extend additional loans,” Nomura said.

This would also mean an improvement in credit deposit ratio to a near normal level of 75 per cent, from 72.6 per cent in mid-October and would “tighten banking system liquidity incrementally,” Nomura said.

The implication of this is hardening of bond yields. From 6.41 per cent in end-July, the yields on the 10-year bond have risen to 6.94 per cent and bond dealers expect the yields to cross the seven per cent mark quite soon.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in