"As Trump trade fades, investors reverse course")

The Trump trade is over. Get ready for “Trump Lite.” Developing doubt about the U.S. administration’s ability to deliver on its pro-growth policy agenda—at least any time soon—has upended a strategy that had been a winner since November’s U.S. election: sell bonds, buy the U.S. dollar and pick up cheap stocks that might benefit from improved U.S. growth.

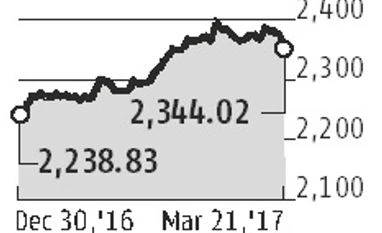

That trade went into reverse in Tuesday’s U.S. trading: The S&P 500 fell 1.2%, its first decline of more than 1% this year and biggest drop since October, while the ICE U.S. dollar index, which tracks the dollar against a basket of six currencies, slipped below 100 for the first time since Feb. 6.

But even before the reversal there had been weeks of stall. In fact, a more successful strategy this year than the Trump trade has been to discount a U.S. recovery and bet instead on Europe and Asia, particularly China. The MSCI Emerging Markets Index is up 8.6% in 2017—driven by double-digit gains in Turkey, China, Hong Kong and India—trumping the S&P 500’s 4.7%. Even European stocks have outperformed the U.S. over the past month, despite concerns around France’s coming election.

That trade went into reverse in Tuesday’s U.S. trading: The S&P 500 fell 1.2%, its first decline of more than 1% this year and biggest drop since October, while the ICE U.S. dollar index, which tracks the dollar against a basket of six currencies, slipped below 100 for the first time since Feb. 6.

But even before the reversal there had been weeks of stall. In fact, a more successful strategy this year than the Trump trade has been to discount a U.S. recovery and bet instead on Europe and Asia, particularly China. The MSCI Emerging Markets Index is up 8.6% in 2017—driven by double-digit gains in Turkey, China, Hong Kong and India—trumping the S&P 500’s 4.7%. Even European stocks have outperformed the U.S. over the past month, despite concerns around France’s coming election.

“There’s a lack of confidence in the reforms and the overall policy agenda, and that’s been spoken about underpinning the whole market sentiment and animal spirits so far,” Catherine Yeung, investment director at Fidelity International, said about investors’ reconsideration.

The skittishness spilled into Asia Wednesday. Japan’s Nikkei 225 Stock Average fell 2.1% to 19183.27, erasing all its gains for the year. The yen strengthened to as much as ¥111.4350 to the dollar; a strong yen typically hurts the earnings of Japanese exporters. Shares also struggled in Hong Kong, with Chinese companies particularly hard hit.

Increasingly, investors are showing they believe the Trump trade has got out of hand. Around one-third of portfolio managers believe global equities are overvalued, the highest level on record going back to the turn of the century, according to Bank of America Merrill Lynch’s monthly survey of 200 funds managing $592 billion, and around four-fifths believe U.S. stocks are the most overvalued of all. Around a third believe the U.S. dollar is overvalued, the highest level since June 2006.

The “Trump Lite” trade hinges upon the administration’s getting sandbagged in policy fights, such as the current wrangling over health care. Drawn-out congressional debates over the details of stimulus measures could cause inflation to peter out, encouraging investors to resume the hunt for yield—buying bonds and stocks with sustainable dividend income.

From the start the market had been too optimistic about Donald Trump’s ability to execute the finer details of his economic policy, said Megan E. Greene, chief economist at Manulife Asset Management.

“The risks were always going to become more balanced in the markets as it became apparent how aggressive and difficult the administration’s policy agenda is this year, with limited legislative days remaining in the calendar,” she said. “There is little doubt some stimulus will come through, but it is likely to be smaller and take longer to hit the real economy than many investors would like to believe.”

But if Mr. Trump’s current woes are bolstering emerging markets, he still has wide scope to spoil the party, particularly by pushing on his campaign pledges to get tough on the U.S.’s trade partners.

“The market seems to have forgotten about the rhetoric Trump has talked about regarding trade,” said Fidelity’s Ms. Yeung.

The skittishness spilled into Asia Wednesday. Japan’s Nikkei 225 Stock Average fell 2.1% to 19183.27, erasing all its gains for the year. The yen strengthened to as much as ¥111.4350 to the dollar; a strong yen typically hurts the earnings of Japanese exporters. Shares also struggled in Hong Kong, with Chinese companies particularly hard hit.

Increasingly, investors are showing they believe the Trump trade has got out of hand. Around one-third of portfolio managers believe global equities are overvalued, the highest level on record going back to the turn of the century, according to Bank of America Merrill Lynch’s monthly survey of 200 funds managing $592 billion, and around four-fifths believe U.S. stocks are the most overvalued of all. Around a third believe the U.S. dollar is overvalued, the highest level since June 2006.

The “Trump Lite” trade hinges upon the administration’s getting sandbagged in policy fights, such as the current wrangling over health care. Drawn-out congressional debates over the details of stimulus measures could cause inflation to peter out, encouraging investors to resume the hunt for yield—buying bonds and stocks with sustainable dividend income.

From the start the market had been too optimistic about Donald Trump’s ability to execute the finer details of his economic policy, said Megan E. Greene, chief economist at Manulife Asset Management.

“The risks were always going to become more balanced in the markets as it became apparent how aggressive and difficult the administration’s policy agenda is this year, with limited legislative days remaining in the calendar,” she said. “There is little doubt some stimulus will come through, but it is likely to be smaller and take longer to hit the real economy than many investors would like to believe.”

But if Mr. Trump’s current woes are bolstering emerging markets, he still has wide scope to spoil the party, particularly by pushing on his campaign pledges to get tough on the U.S.’s trade partners.

“The market seems to have forgotten about the rhetoric Trump has talked about regarding trade,” said Fidelity’s Ms. Yeung.

Source: The Wall Street Journal

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in