"Aditya Birla Capital: Advantage of a financial conglomerate")

There are quite a few conglomerates in India, but very few in the financial services space. The listing of Aditya Birla Capital (ABCL), however, offers an option to investors in a space largely dominated by HDFC, Reliance Capital and banks such as ICICI, Axis and State Bank of India.

While Aditya Birla Capital may not seem to have had an exuberant debut on Friday, with its stock hitting the lower-end of the circuit filter (meaning there were no buyers) and closing at Rs 248.15, it is more of a technical issue due to realignment of a global index following ABCL’s separate listing. Some profit-booking by investors who were allotted ABCL shares is also not ruled out given the surge in valuations in last two months.

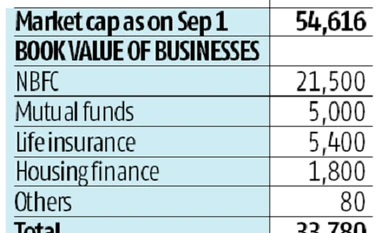

Long-term investors, however, wanting to mop up shares of a scalable financial services firm could still consider the stock once it settles. Post-listing, ABCL’s market capitalisation (m-cap) of Rs 54,616 crore makes it the 53rd most valuable company in India, slightly ahead of Hindalco. The latest m-cap, though much higher than the market value of Rs 32,000 crore in end-June when PremjiInvest bought a 2.2 per cent stake in ABCL, indicates that the stock still trades at a reasonable 1.6x FY17 price-to-book.

But, what’s more important is that ABCL has presence across key segments such as asset management (AMC), life insurance, housing finance (HFC), and a non-banking finance company (NBFC), all of which are at the right phase of growth and expansion.

The way in which each of the businesses have evolved and how some have undone the mistakes of the past is also interesting. For instance, after suffering an existential crisis in 2010, when regulations pertaining to unit-linked insurance products (Ulips) were overhauled, ABCL’s life insurance business witnessed 30 per cent fall in new business premium in FY11, as 95 per cent of its product offerings were Ulips. It may be noted the event impacted most private life insurance players with the impact varying based on their exposure to Ulips. Embedded value (EV) of ABCL’s life insurance business plunged to Rs 3,220 crore in FY14, from Rs 4,110 crore in FY11. However, EV has now stabilised at Rs 3,430 crore in FY17, with the share of Ulips reducing to 30 per cent, thanks to the constant efforts from the management. Analysts at JPMorgan are confident that the product mix shift towards traditional products and operating leverage should drive earnings improvement.

While the above businesses are fairly old and mature, though improving, its NBFC and HFC are seen as the key drivers. Between the two, the HFC loan book is young and unseasoned. Until now, it has had high dependence on employees of the Aditya Birla group companies, though the loan book has expanded to Rs 4,136 crore in FY17, from Rs 142 crore in FY15 (year of commencement).

NBFC operations under Aditya Birla Finance is ABCL’s marquee entity. Not only has its loan book rapidly expanded to Rs 34,700 crore in FY17, from Rs 1,000 crore in FY10, its relevance to ABCL’s financials has also increased. Also, 64 per cent of ABCL’s book value draws support from the NBFC. Analysts at Axis Securities believe the NBFC would continue to grow significantly, above the industry trend, recording 25 per cent compounded annual growth in the next five years. “Growth would be driven by product expansion, larger share of loans to small- and medium-enterprises and retail segments and expansion into new geographies,” the analysts add.

Currently, the bias is towards large- and mid-corporates (54 per cent of loan book). Despite this, the asset quality is impeccable. FY14 was the last year of over one per cent gross non-performing assets ratio. Since then the ratio is well under check and stood at 0.5 per cent in FY17. Return on assets at 2.1 per cent and return on equity of 15.8 per cent also augers well.

Overall, with most businesses having good growth potential, the coming years would be interesting from sustainability and scalability perspective.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in