"Crude oil casts a shadow on Dalal Street")

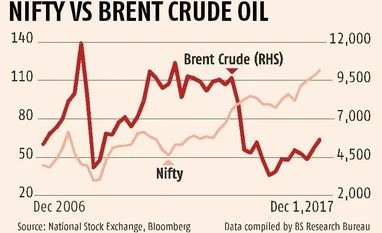

The recent weakness on Dalal Street has raised fears of crude oil’s adverse impact on Indian equities. The benchmark Nifty 50 index is down 3.2 per cent from the lifetime high it hit on November 3. In the same period, Brent crude oil is up 1.9 per cent and hit a new 52-week high. This also suggests the Indian markets are now struggling to hit fresh highs as oil prices inch up. In stock market parlance, every rally is being sold into by long-term investors, creating fear of a major market correction if oil prices rise any further or if the news cycle worsens.

“Higher crude oil prices are negative for the Indian economy in general and the equity market in particular by way of its adverse impact on corporate earnings. Lower crude oil prices since 2014 has been a bonanza for the Indian economy and corporates and there is a fear of this now going away,” says G Chokkalingam, founder and managing director, Equinomics Research & Advisory.

Historically there is a negative correlation between international crude oil prices and Indian equity markets. For example, the big market crash in 2008 when the benchmark index more than halved in less than a year after hitting a lifetime high in early 2008, was preceded by a period of rising crude oil prices. Brent crude oil touched an all-time high of nearly $140 a barrel in the middle of 2008 after rising all through 2007 and early 2008. Similarly, the post-Lehman crisis recovery in equities commenced within weeks of crude oil prices crashing to nearly $40 a barrel in December 2008. The recovery was interrupted as crude oil prices began to spike beginning early 2010.

The current rally, which has seen the benchmark index nearly double from the lows of June 2011, has been accompanied by a steady fall in crude oil prices from their highs in June 2014. The current calendar year has been one of the few in recent years when both equity and crude oil did well. The Nifty 50 is up 24 per cent during the current calendar year while crude oil prices are up 15 per cent during the period.

Experts attribute this to the inverse relation between crude oil prices and India’s macroeconomic ratios. Higher oil prices translate into bigger fiscal and current account deficits that puts pressure on rupee-dollar exchange rates, hurting foreign portfolio investment in equity markets. At the corporate level, it pushes up energy and raw materials cost. For example, the country's top listed companies are estimated to have saved nearly Rs 15 lakh crore in the last few years on account of lower raw material and energy costs, boosting their profits by nearly 40 per cent during the period. Nearly 80 per cent of these gains accrued in the last three years when oil prices began to decline, beginning June 2014. Even a partial roll-back of these gains would be negative for corporate earnings, going forward.

Bulls however see a cap on crude oil limiting its adverse impact on the Indian economy and markets. “If oil prices do spike, you can see more drilling in US and Russia of shell oil which will offset the price rise. It can go to $70 or $75 due to cost inflation but $100 seems hard unless there is some epic geopolitical shock hitting supply from a major oil producer,” says Andrew Tilton, chief Asia-Pacific Economist, Goldman Sachs.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in