"Dalal Street sees strong recovery for Apollo Hospitals; stock rises")

While other listed hospital stocks are struggling on the bourses, Apollo Hospitals has been hitting 52-week highs in recent weeks. The company has been an outlier among peers on expectation of better utilisation and performance in the hospitals business and value unlocking through monetisation of its pharmacy business.

The latter business is India’s largest, with over 3,000 stores and a standout segment in recent years. It was a prolonged weak earnings phase emanating from an aggressive expansion plan that had been responsible for earlier underperformance.

With earnings recovery taking root from the second half of 2017-18, and improvement in each quarter since, the Street is taking notice of the scale and margin improvement.

This is reflected in the stock gaining 47 per cent since July lows, outperforming peers and the BSE healthcare index that is up about 2.3 per cent during

the period.

The healthcare services business’ improvement is being led by growth in mature hospitals’ profit and by the new hospitals cluster. In the September quarter, revenue from health care or the hospital business grew 11 per cent year-on-year, led by a 23 per cent and 9 per cent rise in new and existing hospitals, respectively. The pharmacy business jumped 23 per cent.

Apollo also continued to cut losses on segments Cradle and Spectra. Operating loss in the first half of 2018-19 for the two units are down by half. The management says it is on track for break-even in 2020.

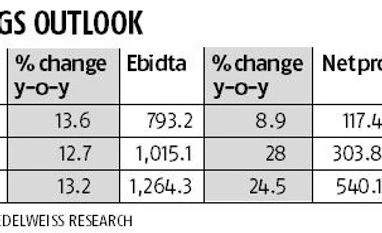

With the financial year's first half seeing improvement, expectations high for the December quarter. Analysts at Edelweiss expect it to be led by the hospitals segment, as key loss-making ventures break even. They think Ebitda would rise 17 per cent over a year. Elara Capital expects revenue to grow 14 per cent year-on-year, accompanied by Ebitda growth of 17 per cent.

With these adding to the operations at the consolidated level, the company is on track to achieve break-even in its AHLL (Cradle and Spectra). Also, with capital expenditure moderating, analysts expect the return on capital employed to rise from seven per cent to 15 per cent over FY18–21.

Value unlocking in the pharmacy business is also keeping investors enthused. The company is de-merging its pharmacy business into Apollo Pharmacy, to comply with foreign direct investment rules, which prohibit the latter in pharmacies.

There is also a focus on growing the pharmacy business and laying the ground for raising equity or inorganic pharmacy investment, say analysts. The business had been growing well over the past few years and is expected to see annual revenue growth of 18 per cent over FY18-21.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in