"Demand for cement likely to outpace supply in north and east India")

Despite capacity additions in the country’s northern and eastern regions, the demand for cement in these parts is expected to outpace the supply in the next two-three years, leading to shortage. In turn, prices are expected to firm up the most in these two regions.

In the recent past, prices in the western part of the country rose by over five per cent followed by north, where it increased by three per cent. In the central region, which is dotted by numerous limestone reserves, prices were up by two per cent. However, cement prices in south and east India declined by two and three per cent, respectively.

A Motilal Oswal report stated cement prices across India were likely to increase by a marginal one per cent on a quarter-on-quarter basis because of the divergent price trends across the country.

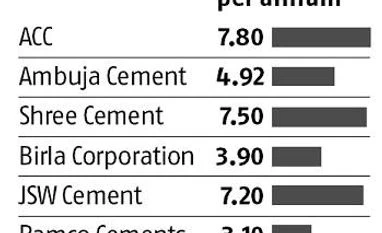

“It is expected that in the next two-three years, the requirement (demand) in the country will grow by 10 per cent as against the current level of 6-7 per cent. Eastern India will grow the fastest,” HM Bangur, managing director at Shree Cement, said.

This comes in wake of major broking houses, including CLSA, raising concerns over the near-term profitability of major cement firms because of the current oversupply, which is affecting prices.

This comes in wake of major broking houses, including CLSA, raising concerns over the near-term profitability of major cement firms because of the current oversupply, which is affecting prices.

Moreover, sand mining issues, muted demand in the real estate sector, transportation costs, and other input cost pressures have left an impact on nearly all the cement majors.

“In two-three years, there is going to be a demand-supply mismatch in the east followed by the north. As a result of supply falling short of demand, prices are expected to recover from the current levels considerably,” Majumdar said.

East India accounts for 19 per cent of the total 471 million tonne (mt) installed capacity while north India accounts for 22 per cent of the total installed capacity.

Industry officials believe at least another 50 mt of fresh capacities are expected to be added during 2018-2021, which will increase the total installed capacity to over 525 mt. Of the new additions, 24.5 mt is expected to be added in the eastern region alone.

As and when the per capita income in the country starts to improve from the current level of around $1,600 to touch $1,800, there will be a sudden surge in cement demand at the retail level, reasoned Bangur.

“As people hit this inflection point ($1,800), they will have more disposable income after spending on necessary commodities and luxury items. As a result, with better cash availability, betterment of infrastructure will naturally become a priority and uptake will improve,” Bangur said.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in