"Don't panic if there's a downgrade in your debt fund")

Debt fund investors don’t need to panic if they suffer interim losses during to rating downgrades of companies in their debt mutual fund schemes. Experts say that as long as the exposure of the fund to such downgraded paper is limited to five-seven per cent, there should be no reason to get too worried. “Most think that debt funds are risk-free. If they give you better returns than a bank fixed deposit, they have to take more risk,” says Kunal Bajaj, founder and CEO at Clearfunds.

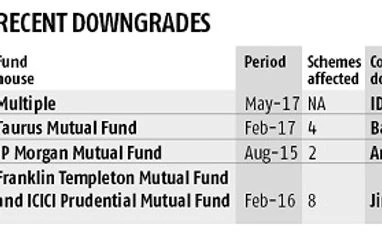

Recently, rating agencies downgraded IDBI Bank, which would have resulted in mark-to-market losses for mutual funds. But fund managers are little worried about it as their exposure is limited to the issuer and also because the bank is backed by the government. But if a scheme has a high exposure to a company facing downgrade, investors should consider their options. In February, when rating agencies downgraded Ballarpur Industries, Taurus Asset Management’s four debt scheme suffered losses. At that time, three schemes had exposure of over 11 per cent to Ballarpur Industries.

How much risk an investor should be willing to take in debt depends on his investment tenure. Medium and long-term debt investors with a horizon of over three years, have no choice but to put up with volatility. In categories such as credit opportunities fund, there’s always risk of downgrades as fund managers take exposure to papers that have lower ratings but give higher returns. In dynamic bond funds the returns could fall 1-2 per cent in a day if a fund manager’s call on interest rates goes wrong. If investors cannot stomach volatility, they should look at bank fixed deposit or other fixed income instruments.

Those investing for short-term – up to two years – need to be more cautious when selecting a fund. “As interest rates started bottoming out last year, some debt funds have been investing in riskier papers for higher returns. In short term funds, fund managers should not take credit or duration risk,” says Vidya Bala, Head of mutual fund research at Fundsindia.com.

Bala suggests that when selecting an ultra-short-term or a short-term fund, investors should avoid schemes that have given returns higher than the category average. “Higher returns show that the fund manager took unwanted risk,” says Bala. When long term funds, such as credit opportunity, opt for riskier papers they usually put processes in place to recover money in case of defaults. Mutual funds take collateral from borrowers in such cases. It could be an asset or shares of a group company or a project generating cash flows. In short term debt funds, similar safety measures are usually not sought.

For a retail investor, it’s not easy to analyse the portfolio of a debt fund. Experts say the only option is to stick with larger fund houses. In case of short term funds, opt for those who have returns close to the category’s average. Always match your investment horizon with that of average portfolio maturity of the scheme. If an issuer in your debt fund scheme is downgraded, give the fund house at least three months to tackle such problems.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in